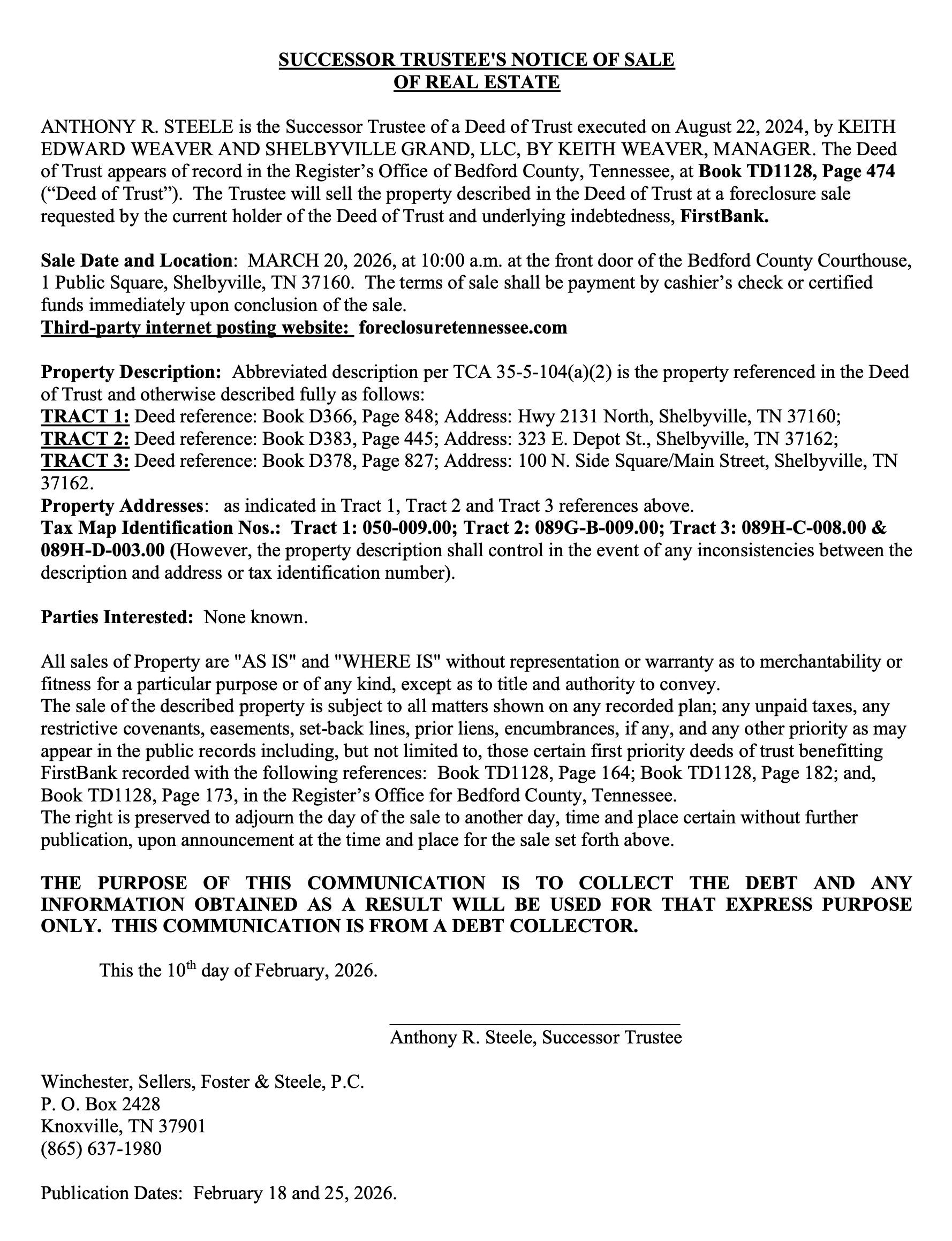

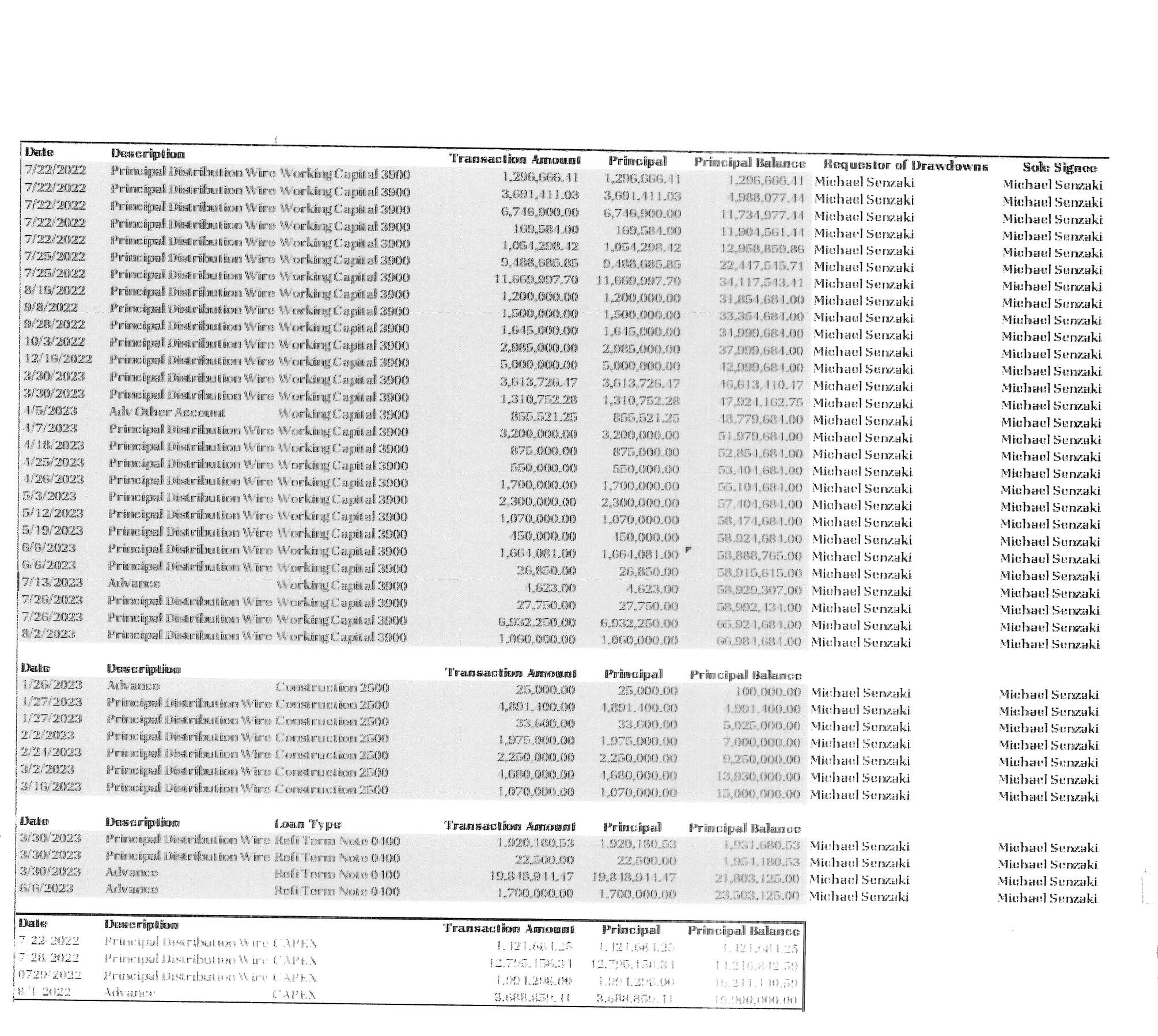

Uncle Nearest Receivership & Lawsuit : LIVE UPDATES

FOLKS I HAVE TO CLOSE THIS PAGE. IT’S BECOME UNEDITABLE. I have apparently broken Squarespace with so many words and cats.

Here’s the link to the new one.

Been like this a couple of weeks due to the amount of content on one page.

This WAS the LIVE UPDATE page for the ongoing saga of the Uncle Nearest Receivership which was ordered on 8/14. If you haven’t been following along, please check out this piece first. It’s a decent breakdown of how we got here. This piece here will be heavily seasoned with opinions, thoughts, and commentary and that will be italicized.

If you feel like sharing your story or have any tips feel free to contact me here. Your anonymity and confidentiality will be respected.

Bye Kelli, we hardly knew ye.

Fan mail from Keith. :)

The hits just keep on coming for the successful business.

I’m laughing so hard I have a tiger growing out my armpit. Also, Hi Kelli!

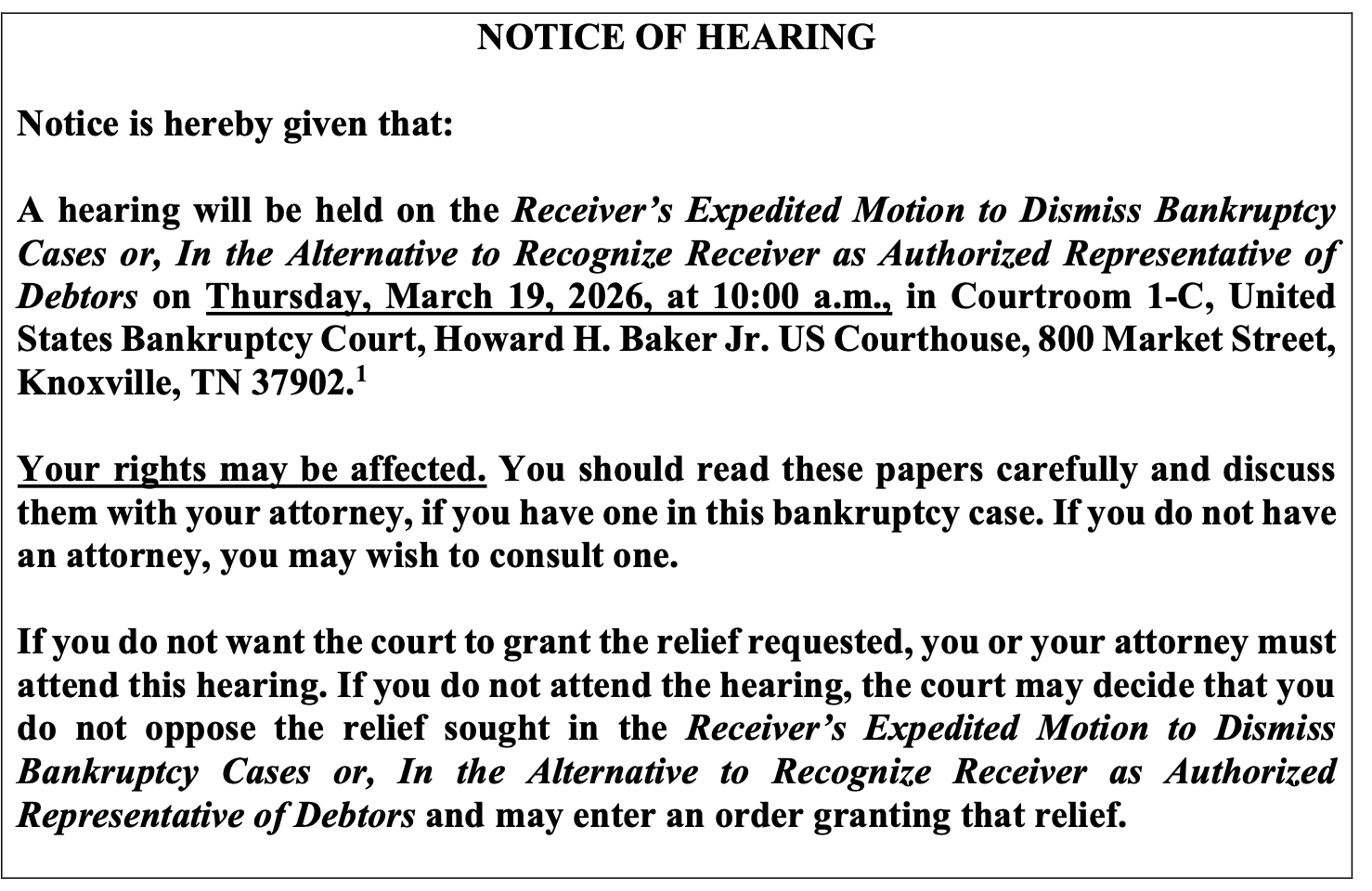

UPDATE #2- 3/18-

The Weaver (TM) is in New Orleans right now. She’s currently signing dusty bottles in front of no one at my locals. She’s also at a dinner Friday night at Brennan’s. Good food, bit of a safe choice, there are better options.

Anyway, flurry of filings in the bankruptcy docket, but it’s mostly procedural stuff.

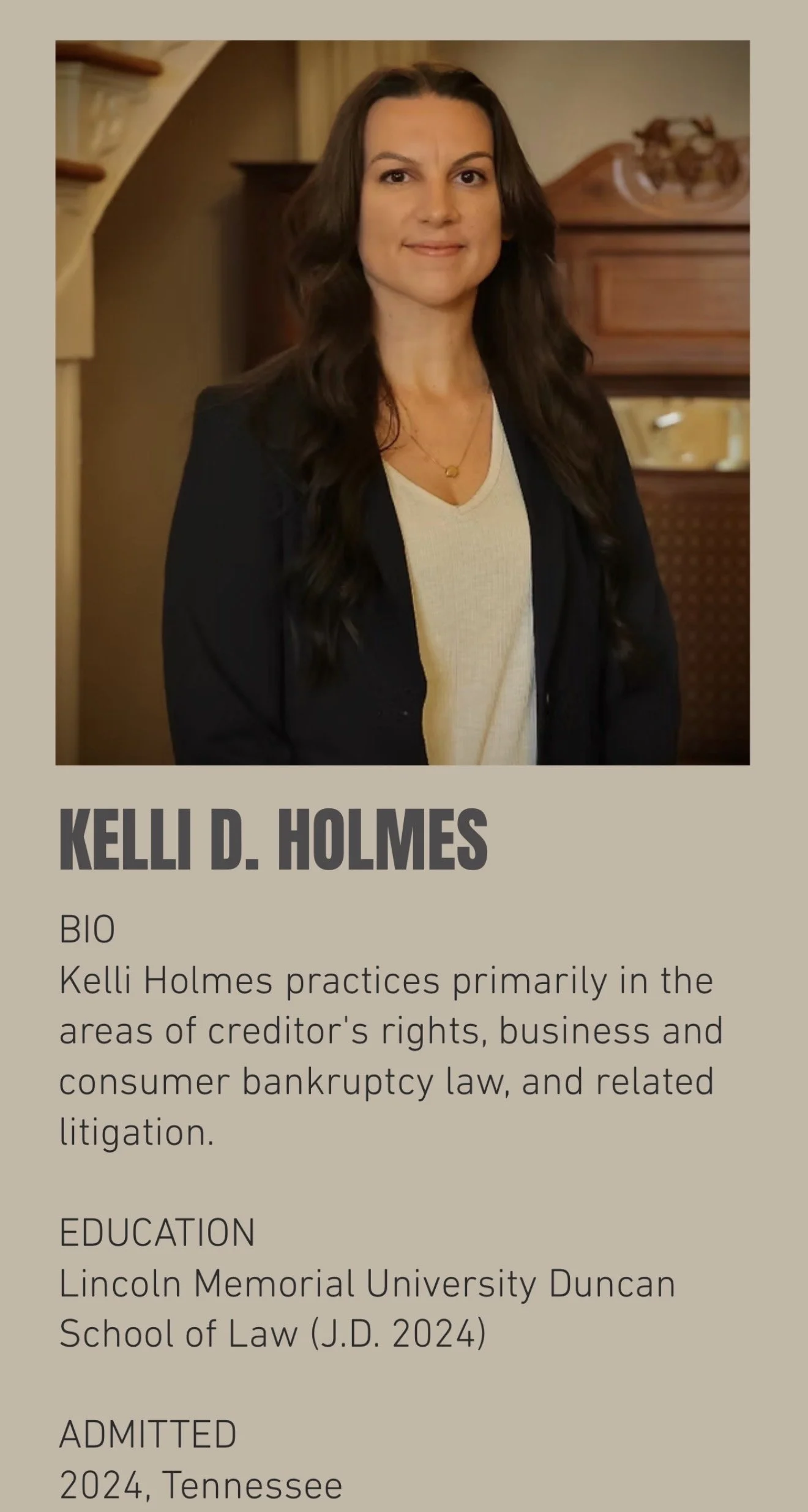

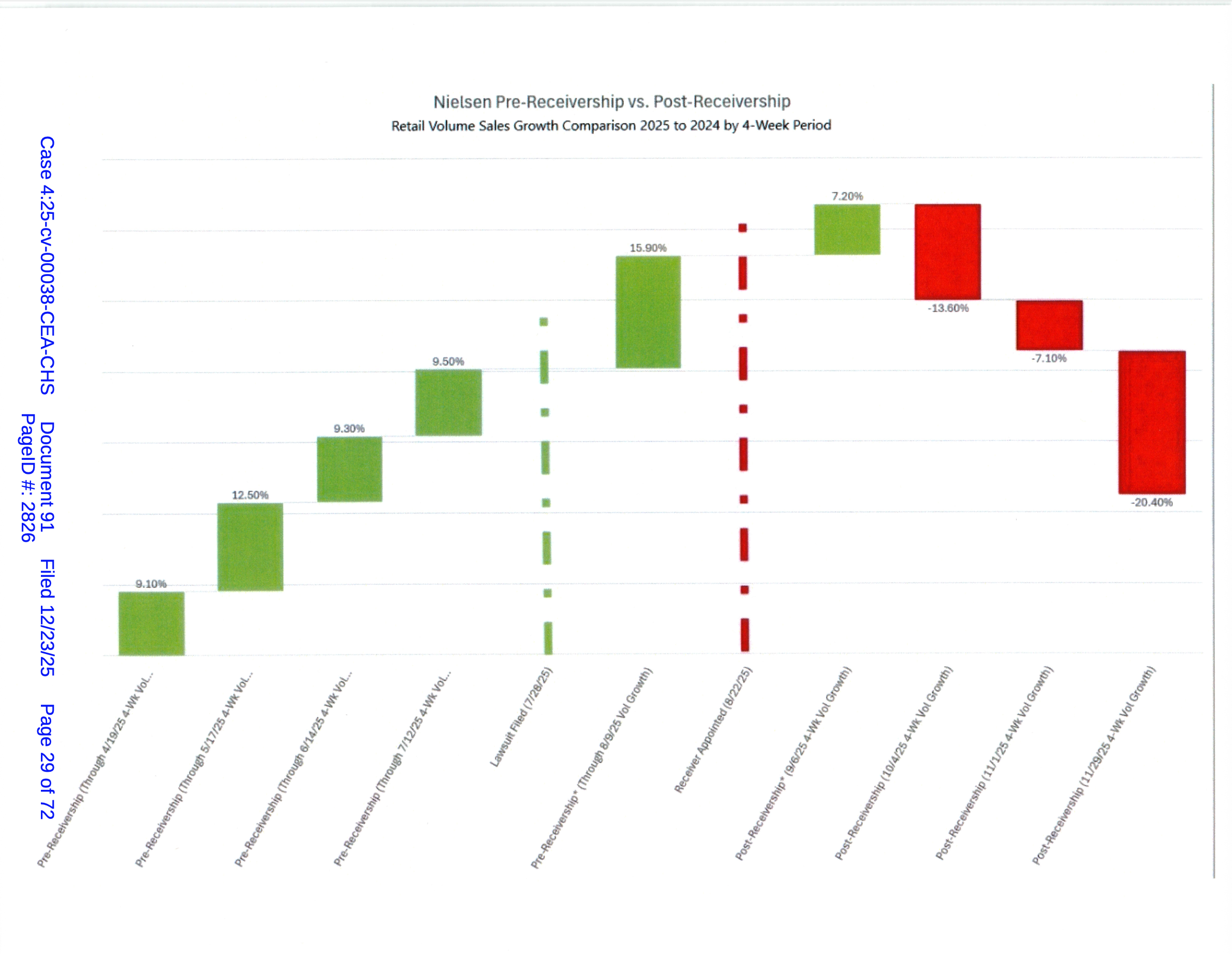

Everyone say hello to Kelli, she’s the newest lawyer to become embroiled in The Great Uncle Nearest Nonsense.

UPDATE 3/18-

I’m gonna start with don’t ever fuck with Phil. This receiver must be big mad, as he was in court yesterday filing, and this morning another huge dump of documents filed to the Bankruptcy court. I apologize for not having the time to break each one down as normal, but this week is insane for me. I have a few highlights for you anyway starting with a rumor.

Did The Weaver (TM) close on a property sale while everyone was going through all these filings?

Did you know that Fawn emailed the team saying the receivership was over?

Cap’N Phillip filed a motion for dismissal in the bankruptcy court asserting that he has “exclusively vested power” to run Uncle Nearest, and he alone, per the order to install a receiver.

He said, that if the motion to dismiss is not granted, then he must be installed to represent UN.

Cap is probably big mad at the waste of time here, but also probably smirking as he filed.

Cap also said he’s ready for Court if the motion for expedited hearing is granted.

Cap calling bluffs.

“Fawn Weaver does not have authority under Tennessee law to file bankruptcy petitions on behalf of the Receivership Entities. That authority rests solely with the Receiver pursuant to the clear and unequivocal terms of the Receivership Order entered by the District Court. Fawn Weaver acted unlawfully and without any corporate authority when she signed and filed bankruptcy petitions in this Court on behalf of the Receivership Entities. Accordingly, this Court lacks subject matter jurisdiction to administer these bankruptcy cases.”

This was always going to be the crux of the argument. Does she have authority? No. This case will be dismissed.

“A number of courts have found that a bankruptcy filed for the purpose of relitigating a receivership order, or derailing a receiver’s administration of an estate, constitutes bad faith and is cause for dismissal.”

“Fawn Weaver has not attempted to hide the true purpose of these filings. Immediately after filing these cases, she published a press release announcing that these bankruptcy filings brought “the court-appointed receivership to an end.”

“Once this Court reaches that decision, it must either dismiss the case or convert it to one underChapter 7.”

“Alternatively, if the Court determines that these cases should not be dismissed, the Receiver respectfully requests that the Court enter an order declaring him to be the exclusive authorized representative of the Receivership Entities (the debtors herein).”

It’s almost like someone who specializes in bankruptcy cases might know how these things work. If only The Weaver (TM) knew that her choice of Receivers, was going to be the one who ended up metaphorically burying her.

Cap is ready to go tomorrow freaking morning.

UPDATE #2- 3/17-

A very, very wise man once told me that there is a lie in every single thing that The Weaver (TM) says. It doesn’t matter if it’s in court, on socials, in person, on TV, it really doesn’t matter who you are, if she’s talking to you, she’s lying about something. When I saw the video this morning, my first thought was about like everyone else’s upon seeing it, WHAT THE FUCK?!

Fortunately before she started listing all the bankrupt companies like a Ripped Fuel loaded Wikipedia article, I remembered what he said. So even though the shitass that sent me the fan mail wanting to see my face (posted below for the lulz), my surprise didn’t last long, because like any Weaver statement or filing, it seldom holds up to any real scrutiny.

The first tell was the Press Release, sent by Grant Sidney. The lawsuit against the bank was the second, because the complaint was nothing more than rehashed stuff that was filed in this case already. The third tell was her mouth was moving.

I told everyone to take a deep breath, and hopefully you did, because the receiver answered, as I assumed that he would (he was fast though, I didn’t expect that). Let’s break it down.

Are you not Catertained?

RECEIVER’S EXPEDITED MOTION FOR SANCTIONS

“Phillip G. Young, Jr. (“Receiver”), by and through undersigned counsel, and hereby moves this Court for an expedited order issuing sanctions against Defendant Fawn Weaver and/or her counsel for Ms. Weaver’s wanton and willful violation of this Court’s Order Appointing Receiver.”

Oh Michael Collins, what have you gotten yourself into?

“Pursuant to the Receivership Order, the Receiver is: exclusively vested with: (a) all the powers of officers, directors, members, and/or managers (as applicable) of Uncle Nearest and the Subject Entities to take (or refrain from taking) any and all actions on behalf of Uncle Nearest and the Subject Entities and (b) each of Uncle Nearest’s and the Subject Entities’ rights and powers to act on behalf of any other entity (including as an officer, director, manager, or equity holder), including, without limitation, each Subject Entity, to direct such other entity to take (or refrain from taking) any action in furtherance of the terms under this Order, in each case, until further Order of the Court.”

This is the crux of the entire affair. The Weaver (TM) filed bankruptcy, but can she? The receiver thinks not, and I’ll bet the Judge will agree.

“The Court also enjoined the receivership ntities and “each of their officers, directors, employees, agents, assigns, or any other persons” from “[i]interfering with, obstructing, or preventing in any way, the Receiver’s actions pursuant to this Order, including, but not limited to, any and all actions that may damage the brand and reputation of the Receivership Assets in any form, whether written, verbal, and disseminated through any medium” and from “[i]nterfering in any other way with the Receiver, directly or indirectly.” Receivership Order. Finally, the Court provided that all persons, including employees, officers and directors, “are enjoined and retrained from in any way disturbing, interfering or affecting the Receivership Assets of the administration of the receivership estate.” Receivership Order.”

The Weaver (TM) has been told time and time again to stop pissing in the pool. The pool is a bright gatorade yellow.

“Defendant Fawn Weaver and her counsel have both constructive and actual knowledge of the Receivership Order and its contents. In fact, the Receiver has specifically discussed with both Defendant Fawn Weaver and her counsel the Receiver’s exclusive authority to file for bankruptcy relief on behalf of Uncle Nearest and the Subject Entities.”

I think Michael Collins is about to have a very bad week.

“This Court has previously made abundantly clear to Defendants Fawn Weaver, Keith Weaver, Grant Sidney, Inc., and their counsel the impact of the Receivership Order on their ability to take any action on behalf of the receivership entities. In its Order dated December 22, 2025, the Court struck both a Response filed by Fawn Weaver and Keith Weaver on behalf of the receivership entities and a notice of appearance filed by Manier & Herod, P.C. on behalf of the receivership entities. In so ordering, the Court found that “only the Receiver may represent the Defendant Companies’ interests in this litigation.””

Some people just can’t shut up. I’m pretty stubborn in life, but even I know what a wet newspaper to the beak means.

Good News, the bottles covered in ¼ inch of dust are about to get a glow up.

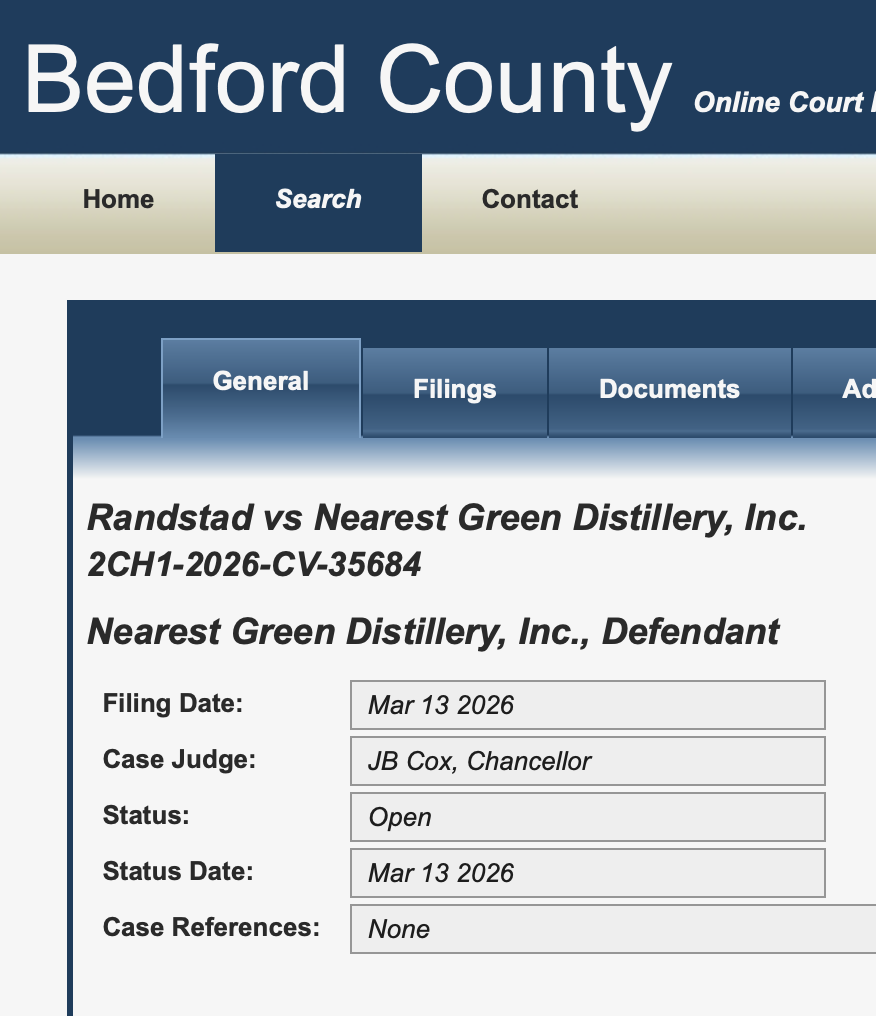

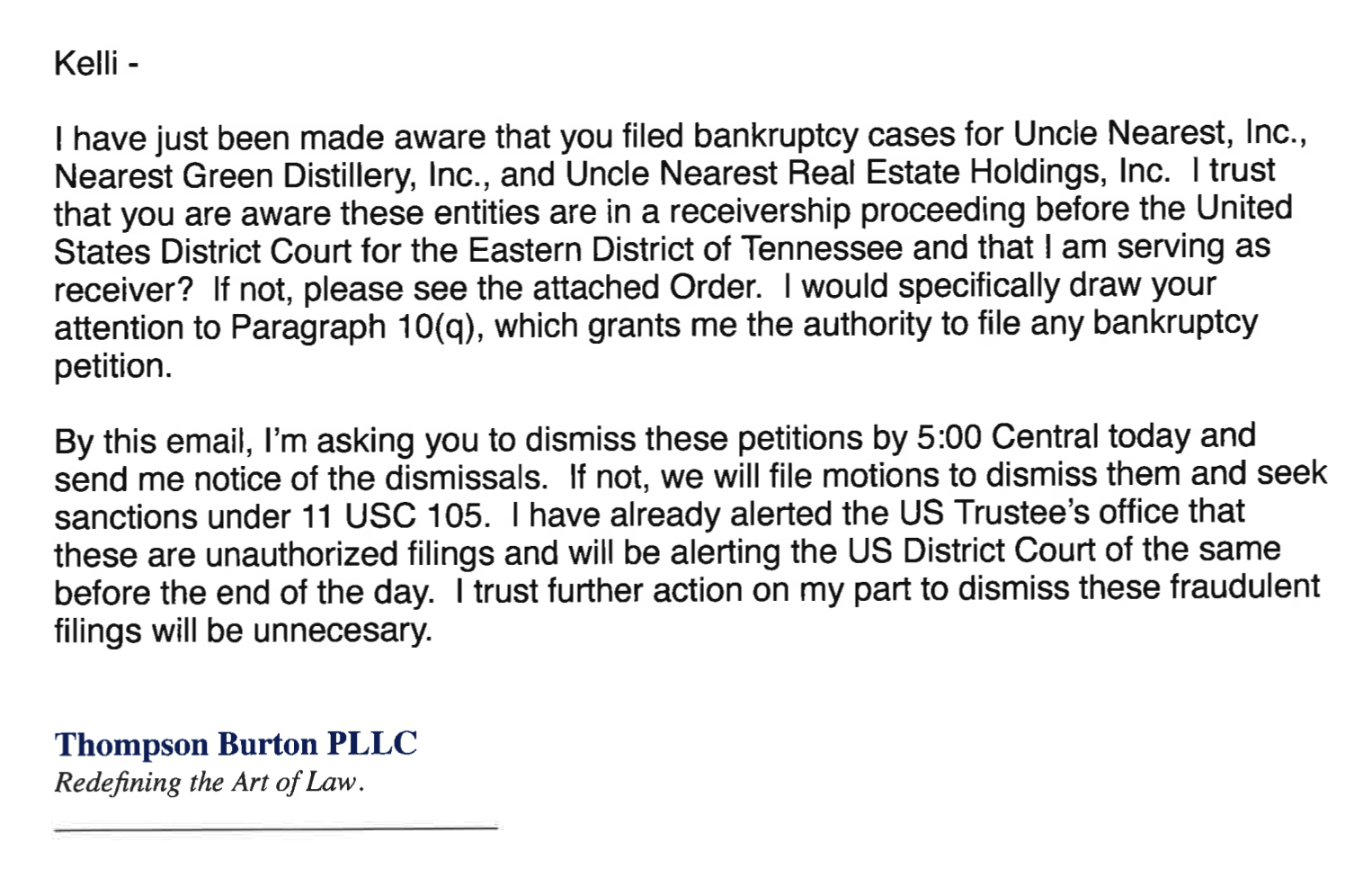

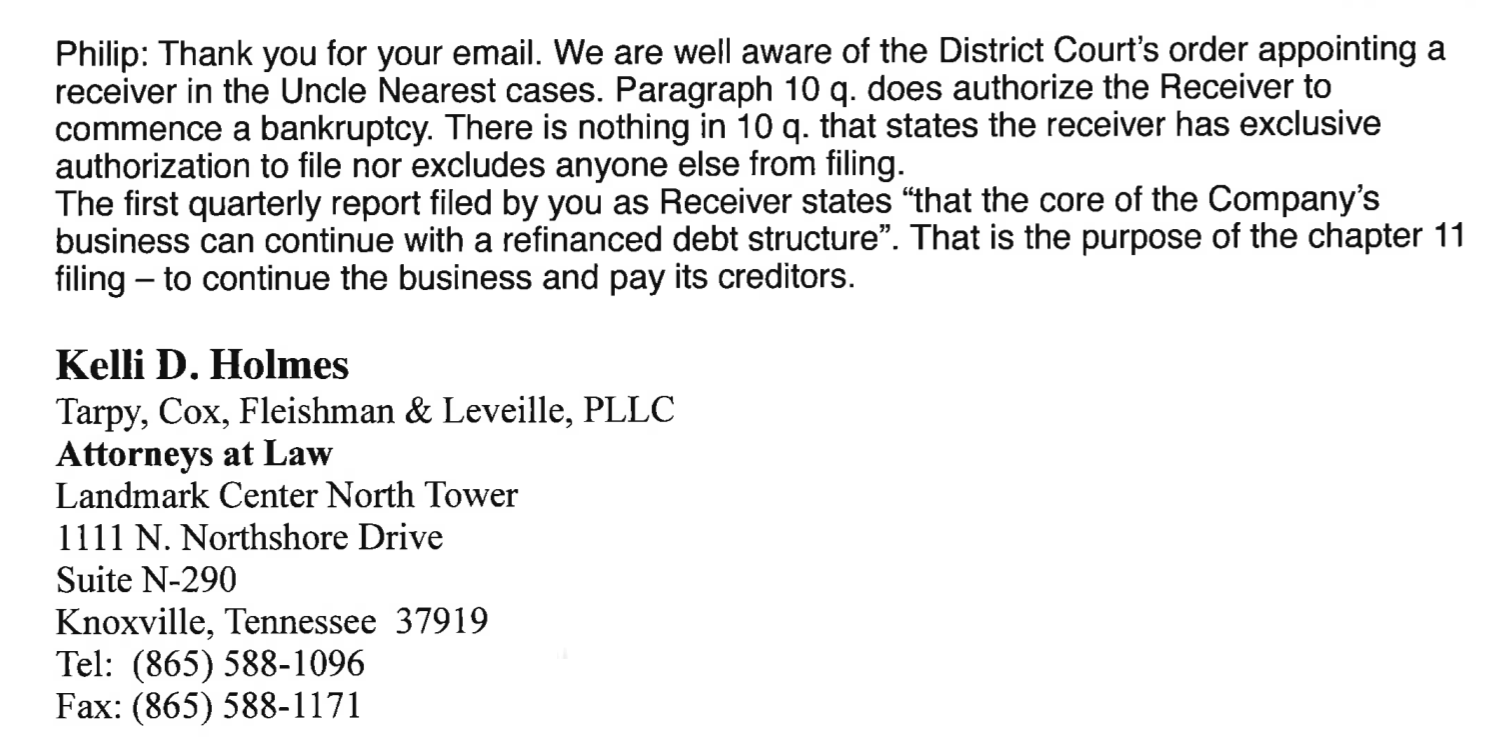

“Despite the clear orders of this Court that the Receiver, and only the Receiver, could act on behalf of the receivership entities, on March 17, 2026, Defendant Fawn Weaver signed and filed bankruptcy petitions on behalf of Uncle Nearest, Inc., Nearest Green Distillery Inc., and Uncle Nearest Real Estate Holdings, LLC in the United States Bankruptcy Court for the Eastern District of Tennessee, Knoxville Division.”

She sure did.

“The Bankruptcy Petitions for these three companies are attached hereto as Exhibit 1. The Receiver forwarded the Receivership Order to these companies’ bankruptcy counsel, Kelli Holmes of Tarpy, Cox, Fleishman & Leveille, PLLC, and asked counsel to dismiss the petition. Counsel responded, saying she was “well aware of the District Court’s order appointing a receiver,” but refused to withdraw the petitions. Emails between the Receiver and Ms. Holmes is attached hereto as Exhibit 2.”

I feel bad for Ms. Holmes, as the odds of her getting paid are about as good as me being declared Admiral of the Turkish Navy.

“Further exacerbating matters, Defendant Fawn Weaver went on a media blitz immediately afterward announcing end of this Court’s ordered receivership. A copy of a press release prepared by Ms. Weaver is attached hereto as Exhibit 3. Ms. Weaver also released a six- minute Instagram video discussing her filing of the unauthorized petitions. A copy of this video can be supplied to the Court upon its request. This follows a troubling pattern about which the Receiver has previously warned this Court, of Ms. Weaver ignoring this Court’s orders to refrain from trying this case in the media and/or social media.”

The Weaver (TM) just stepped on a rake the size of a Ford Expedition by posting that stupid video, and once again, it’s now a court record.

“The unauthorized bankruptcy filings and Defendant Fawn Weaver’s press releases announcing the same has created substantial confusion among Uncle Nearest’s customers, vendors, distributors, employees, and shareholders – not to mention the confusion and trepidation it has caused among potential buyers of its assets. Indeed, within just a few hours after the unauthorized bankruptcy filings, the Receiver received dozens of emails, telephone calls and texts rom various constituents inquiring about how these bankruptcy filings impact the ongoing business of these receivership entities. This has had an immediate and negative impact upon the operation of these businesses.”

This is entirely the point of The Weaver (TM) doing these things Delay, interfere, mess with, and poop in the pool. Everything is about deflections, distractions, and delaying.

“The Receiver and his counsel, in consultation with the United States Bankruptcy Trustee’s office, are taking steps to dismiss the unauthorized bankruptcies of these three companies.”

This man moving quickly.

“However, this Court can and should issue sanctions against Defendant Fawn Weaver and/or her legal counsel as part of its powers to enforce its own orders.”

What’s the over/under on Michael Collins leaving the case?

““Courts of justice are universally acknowledged to be vested, by their very creation, with power to impose silence, respect, and decorum, in their presence, and submission to their lawful mandates.”

Gag order coming.

“Ms. Weaver has continually and consistently violated this Court’s direct orders against trying this case in the court of social media; the Receiver has pointed out these violations previously. These actions, standing alone, are sanctionable. However, today’s unauthorized bankruptcy filings on behalf of Uncle Nearest, Inc., Nearest Green Distillery Inc., and Uncle Nearest Real Estate Holdings, LLC in clear violation of the Receivership Order are beyond the pale.”

I expect, no I demand, more Hamlet from the Judge.

“These actions require immediate and severe sanctions by this Court – not only because they are intentional and knowing violations of this Court’s orders, but because they have caused significant and irreparable damage to the companies that the Receiver has been ordered to protect.”

I cannot for the life of me see how the Judge doesn’t break out the irk stick and wield it frequently here.

Couch cats are the best cats.

“Furthermore, this Court should make clear in a forthcoming order that Defendant Fawn Weaver has no authority to sign a bankruptcy petition on behalf of any of the receivership entities, so that a Bankruptcy Court is not left with the task of interpreting this Court’s order.”

I was just waiting on the inclusion order, but now I get to wait on an order on this too? Dang. Pacer loves my wallet.

“For clarity and transparency, the Receiver has considered filing bankruptcy petitions on behalf of these entities. Indeed, bankruptcy petitions are likely in the future. However, the timing of such petitions relative to the Court’s determination of what entities to include in the receivership, and relative to the process of seeking bids for the purchase of the companies’ assets, is crucial.”

Folks, this is a pretty big admission on cap’N Phillips part. Bankruptcy is likely in the future!

“So too is it critical that the Receiver be empowered to guide the companies through the bankruptcy process. Today’s unauthorized bankruptcy filings are premature and ill-conceived.”

Ill-conceived is putting this very lightly. This was a train derailment.

“Due to the severity and willfulness of the violations of this Court’s Receivership Order, the Receiver would urge the Court to issue severe financial sanctions as a deterrent to ongoing violations of this Court’s orders. The Receiver would suggest a penalty of $25,000 per unauthorized filing, for a total sanction of $75,000 payable to Uncle Nearest, Inc.”

The Weaver (TM) thought she scored a big win when she went on her IG today. It’ll likely cost her more money she doesn’t have.

“The Receiver leaves it to the Court’s discretion regarding whether the sanction should be levied only against Defendant Fawn Weaver or whether it should be jointly and severally payable by counsel in this case and/or bankruptcy counsel who filed the unauthorized petitions with full knowledge of this Court’s orders.”

That Fawn can still command people to do the stupidest of things is very impressive.

Every note from The Weaver (TM) is an L.

“WHEREFORE, the Receiver respectfully requests that this Court enter an Order which:

A. Clearly states that Fawn Weaver is not, and was not, authorized to sign bankruptcy petitions on behalf of any of the receivership entities herein;

B. Issues appropriate monetary sanctions against Defendant Fawn Weaver and/or her legal counsel; and

C. Grants such other relief that the Court deems just and proper.”

I would pay money to see the look on the face of the clown that messaged me when he realizes that nothing has changed.

UPDATE 3/17-

I saw the IG video. I saw the news story that Grant Sidney filed a lawsuit against Farm Credit. I will be seeking that complaint out shortly…. Found it.

Right now, everything is Fawntasyland until we see an order from the court. So take a deep breath.

First of all, the “News” story is a Press Release. I could send out a Press Release declaring myself Emperor of Neptune, doesn’t mean it’s true.

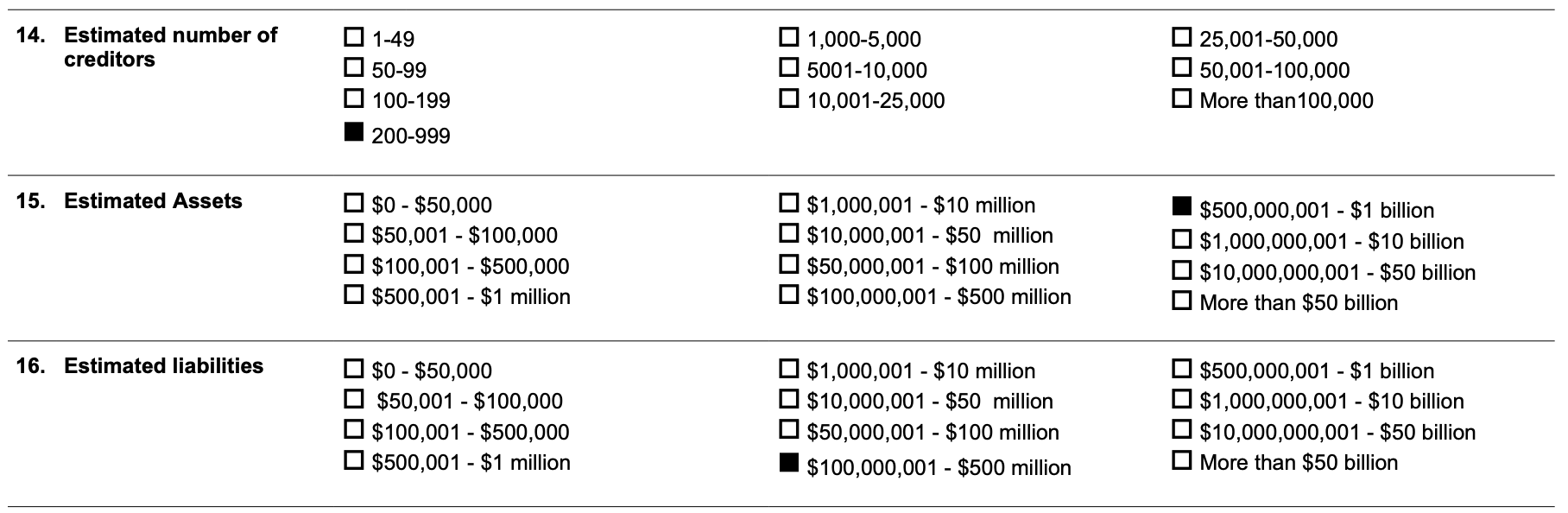

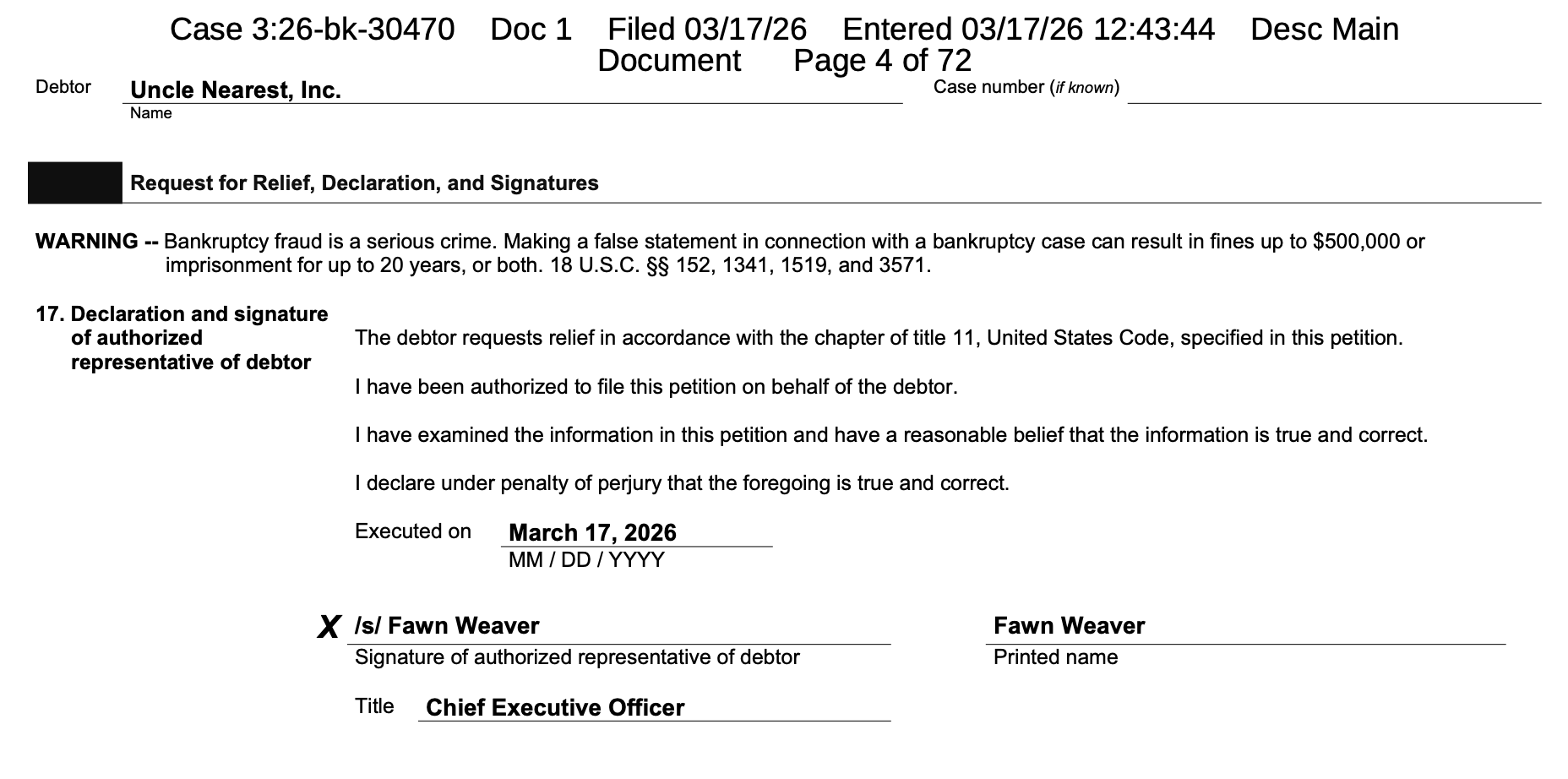

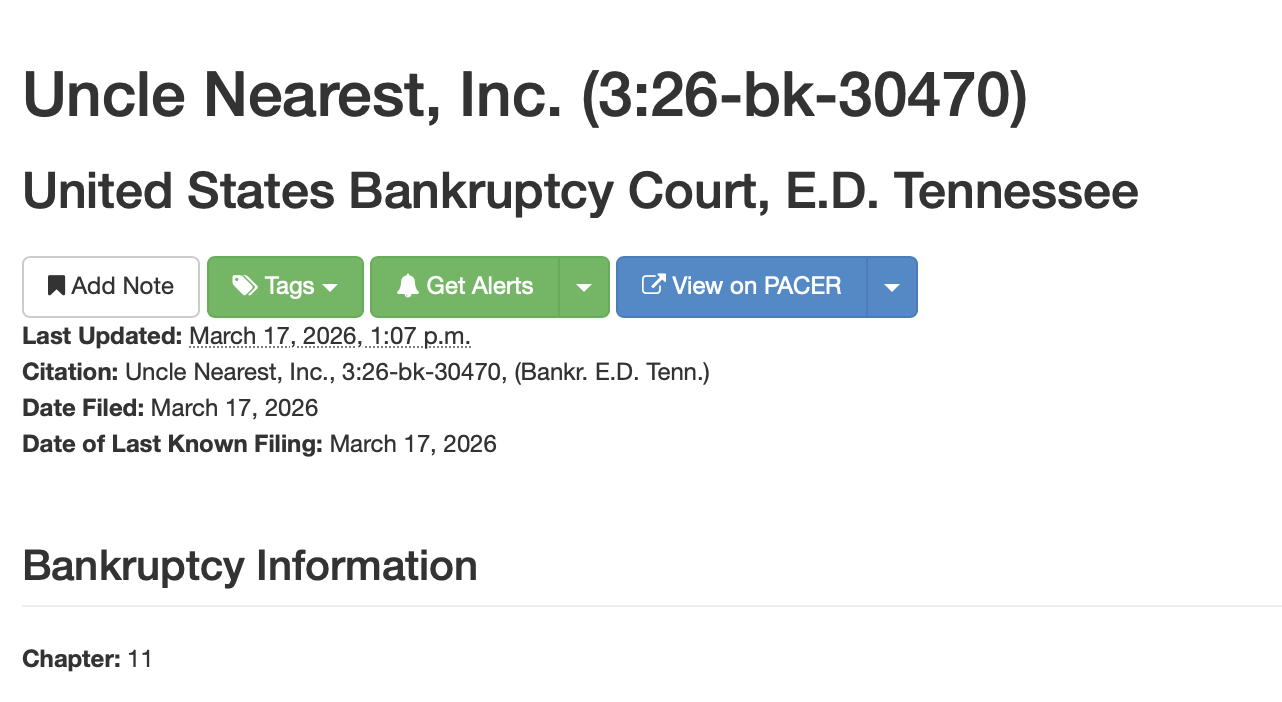

Secondly, Fawn did file bankruptcy for UN. The Court docket info is below. It’s 72 pages (mostly a long list of the creditors), and really just a form. I’ll show some of the highlights too.

Now here’s the thing, she’s not currently the CEO of Uncle Nearest. Can she file this bankruptcy? Yes, she obviously just did. Now whether she has the legal authority to do so will have to be ruled on by the judge.

Does this remove the receivership? Does Fawn regain control? Yes, my phone has been exploding…. Receivership is in place until the court says otherwise. Does she regain control if so? Well, a trustee then essentially becomes a new receiver and off we go again.

Ok, I’m all caught up on the lawsuit in NY from Grant Sidney / Keith / Fawn vs. Farm Credit. Nothing new here. All the same rehashed blame she’s filed in countless other documents. The format is cleaner though, so that new lawyer out there at least knows how to format CatGPT so it doesn’t look like it. But, it sounds like it, so yeah.

Also read through the bankruptcy filing in TN.

Listen.

This is not going to work out for The Weaver (TM) in any meaningful way. This is a rake of epic proportions, and she’s all foot.

The Weaver (TM) still desperately clinging to that 500m-1b valuation. Lulz.

I think someone misspelled Captain Phillip.

Remember folks, Fawn quoted herself in the “press release.”

I have thoughts sometimes. Today is a sometimes kind of day.

UPDATE 3/16-

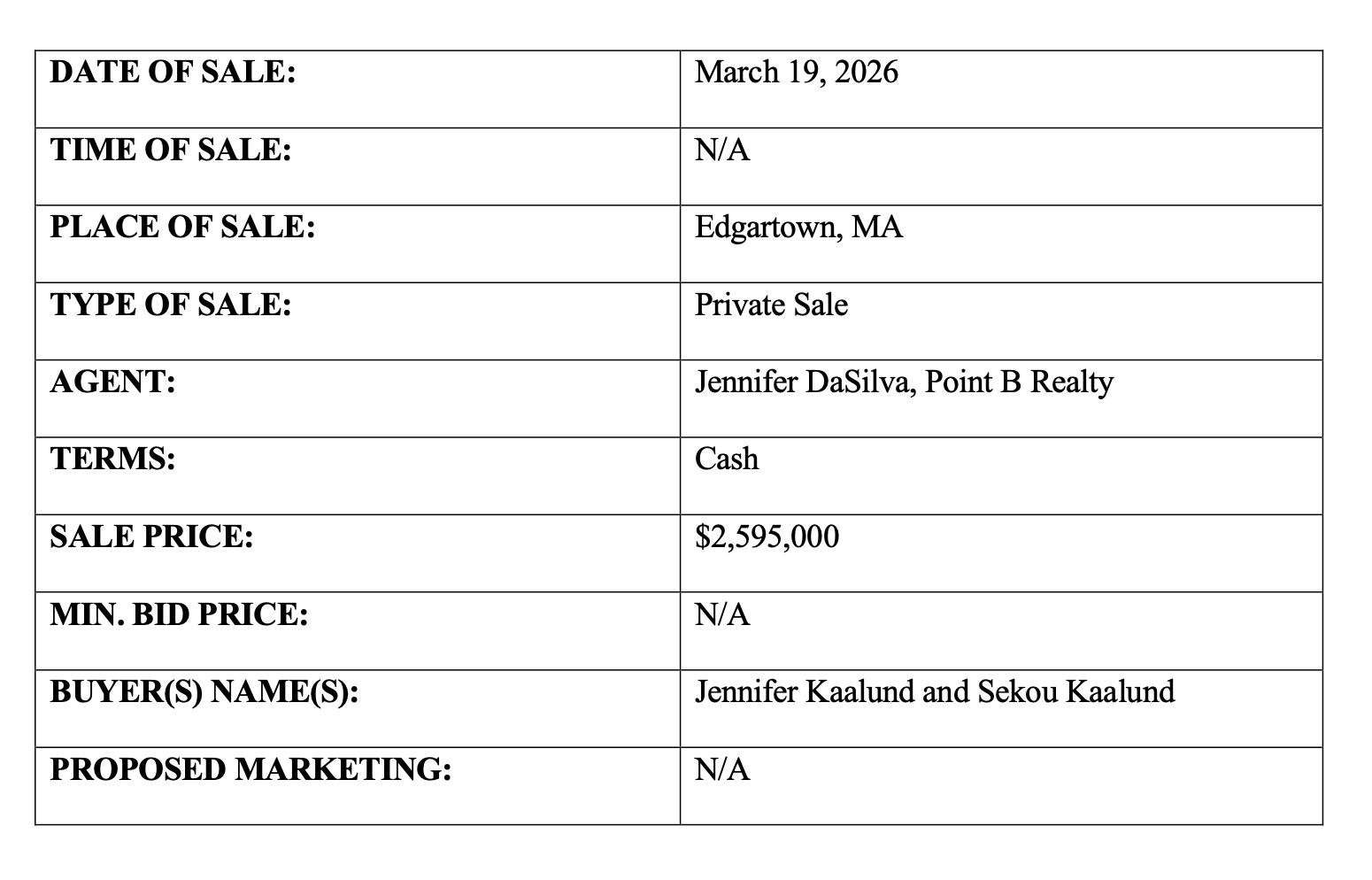

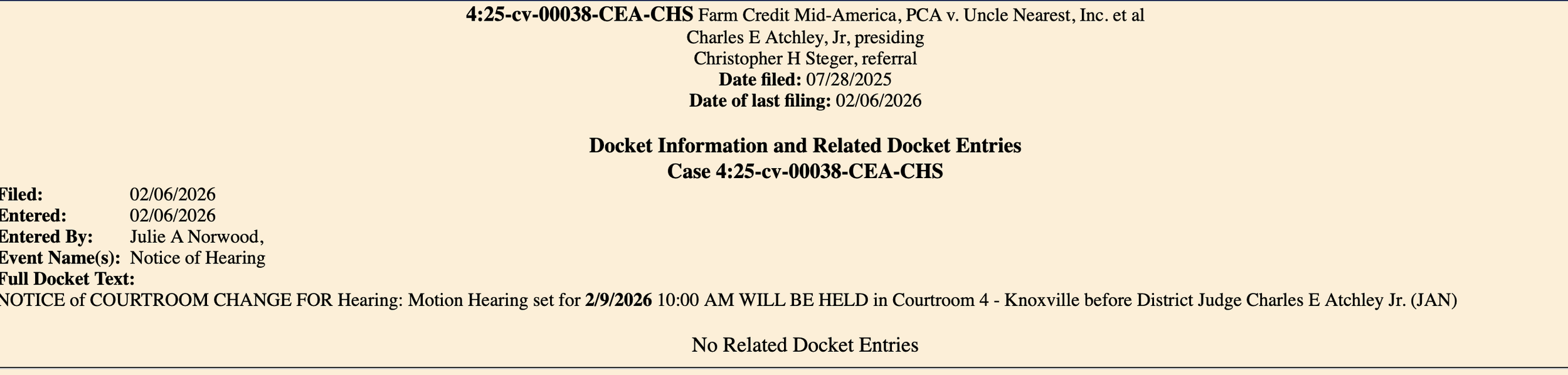

It’s Monday. Since the judge took a week, I expect this week to be bumping. We kick off the day with a Judge’s order on the sale of the Martha’s Vineyard house. Spoiler Alert- it’s paused…

I’ve got a pint of cold brew ready to go, so queue up your favorite MomTok video and let’s dance.

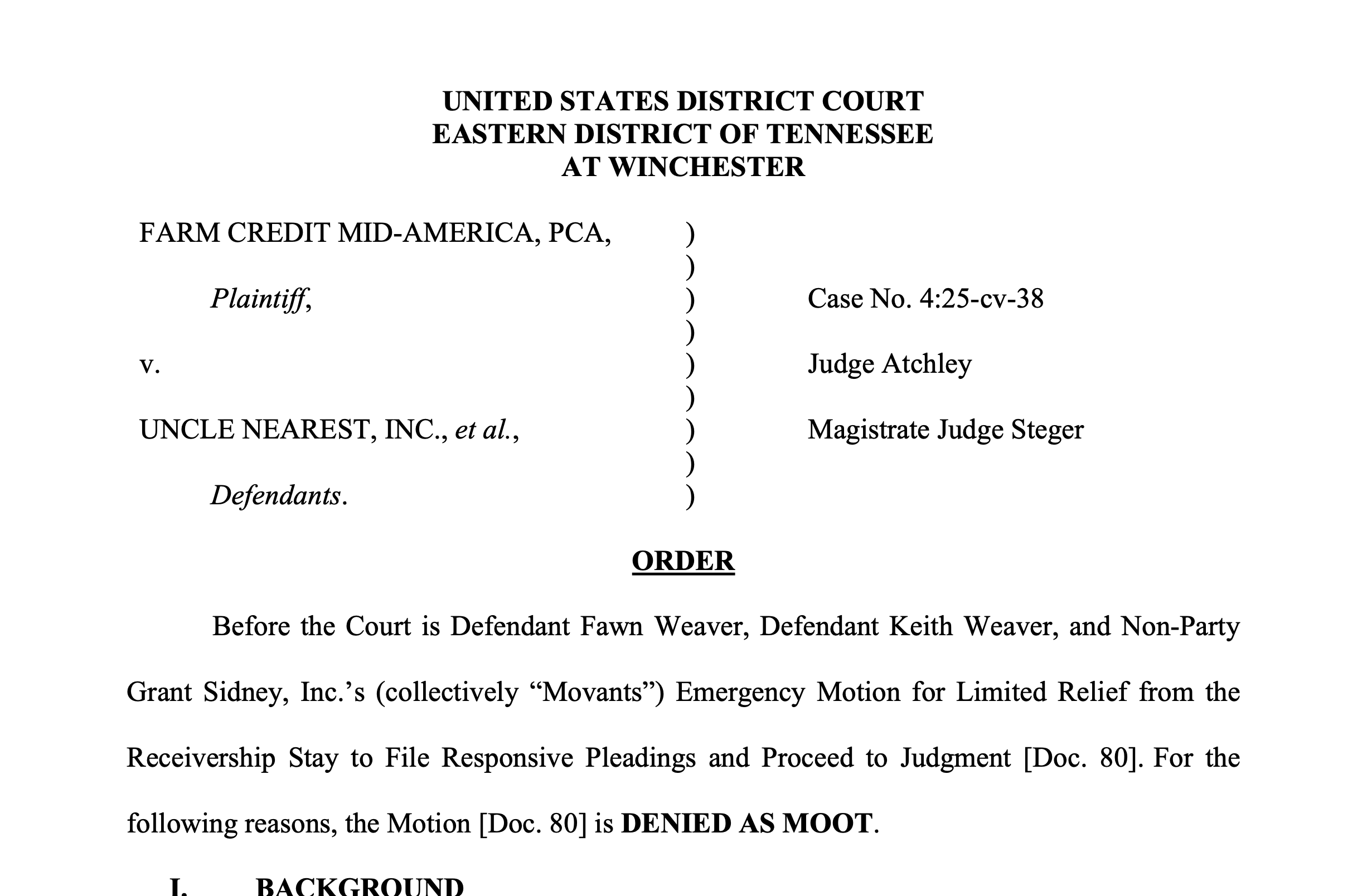

ORDER

“Following receipt of this Motion, the Court ordered expedited briefing, [Doc. 150], and began reviewing the relevant legal authorities governing the sale of property in receivership. This review has revealed that certain statutory pre-sale requirements have yet to be satisfied. Accordingly, the Court will hold the Motion [Doc. 147] in abeyance so that it and the parties may complete these pre-sale obligations.”

The judge must avoid the blood lust of the folks wanting the sale executed quickly (knowing full well the symbolic importance of this house to The Weaver (TM)), and he appears to have done so.

“The Receiver possesses broad power to sell receivership property. This power, however, is not without limits. Title 28, United States Code, Sections 2001 and 2004 govern the procedures a federal court must follow when authorizing the sale of receivership property. Starting with 28 U.S.C. § 2001, it establishes two methods by which a receiver may sell real property.”

I have to say, this might be the most fair judge on the earth, he really has stuck to the law, and skipped the feels.

“First, a receiver may sell real property though a public sale “upon such terms and conditions as the court directs.” These terms and conditions, which the Court has discretion in crafting, “relate[] to such things as setting a minimum price for which the property can be sold, determining whether the property can be sold as separate pieces or must be sold together, [and] whether the property can be sold on credit.” (stating “there is a measure of discretion in a court of equity” as to the “manner and conditions” of a public sale of property). Notably, however, these terms and conditions do not reach the issue of notice. That is governed by 28 U.S.C. § 2002 which provides in relevant part: A public sale of realty or interest therein under any order, judgment or decree of any court of the United States shall not be made without notice published once a week for at least four weeks prior to the sale in at least one newspaper regularly issued and of general circulation in the county, state, or judicial district of the United States wherein the realty is situated.”

Got it. Must post the sale notice in a media form that very few people utilize anymore because the law is very slow to adapt to new forms of media/technology, but hey, the law is the law.

“Second, a receiver may sell real property through a private sale if the Court determines that doing so is in the best interests of the estate. See 28 U.S.C. § 2001(b).1 Such sales, however, are subject to stricter requirements than those governing public sales. Specifically, Section 2001(b) provides: After a hearing, of which notice to all interested parties shall be given by publication or otherwise as the court directs, the court may order the sale of such realty or interest or any part thereof at private sale for cash or other consideration and upon such terms and conditions as the court approves, if it finds that the best interests of the estate will be conserved thereby. Before confirmation of any private sale, the court shall appoint three disinterested persons to appraise such property or different groups of three appraisers each to appraise properties of different classes or situated in different localities. No private sale shall be confirmed at a price less than two-thirds of the appraised value. Before confirmation of any private sale, the terms thereof shall be published in such newspaper or newspapers of general circulation as the court directs at least ten days before confirmation. The private sale shall not be confirmed if a bona fide offer is made, under conditions prescribed by the court, which guarantees at least a 10 per centum increase over the price offered in the private sale.”

This part is directed squarely at the claim of “fire sale” and likely isn’t JUST about the MV house. This will be the judge’s point of view on all assets. Again, the judge is setting clear parameters for the receiver to abide by, as Cap’N Phillip is a court appointed officer, and lays to rest any Ludacris claims of a rush to move assets at a Dollar Store yard sale. (yes, I know how to spell ludicrous).

“The Court cannot waive these requirements, and failure to abide by them can render a sale void. The Court does not have discretion to waive the requirements declaring a receiver’s private sale of real property void where the sale was not preceded by notice, appraisal, and a hearing.”

Yeah, requirements are requirements. Unless you’re a Weaver and you take out massive bank loans, and then just avoid the requirements to pay your loans on time, or contractors, or 1099’s, or employees, or people that rendered services or goods… If only the Weaver’s had run their business like this Judge is running the court.

“In this case, the Receiver seeks to sell the Martha’s Vineyard Property—which contains both real and personal property—via a private sale.. Therefore, the proposed sale is subject to Section 2001(b)’s requirements.2 This means that before the Court can approve the proposed sale, it must (1) appoint three disinterested persons to appraise the Martha’s Vineyard Property, (2) conduct a properly noticed hearing regarding the proposed sale, (3) ensure that the proposed sale price is no less than two-thirds of the appraised value, and (4) see “if a bona fide offer is made, under conditions prescribed by the [C]ourt, which guarantees at least a 10 per centum increase over the price offered in the private sale.” As these statutory pre-sale requirements have not been completed, the Court cannot approve the proposed sale at this time.

I mean that’s fair.

“Accordingly, the Court hereby ORDERS the following.”

Welp, here we go…

“The Receiver’s Expedited Motion to Sell Real and Personal Property in Martha’s Vineyard [Doc. 147] shall be HELD IN ABEYANCE pending completion of the pre-sale requirements listed.”

PAUSED, until due diligence is completed.

“No later than 14 days from the date of this Order, the Receiver SHALL submit a list of at least five proposed appraisers to the Court. This list shall include the proposed appraisers’ qualifications as well as the time they estimate it will take to appraise the Martha’s Vineyard Property;”

I guess Nubian and the other “Friends of” offers will have to wait….

“No later than 5 days from the date the Receiver submits the foregoing list, Plaintiff Farm Credit Mid-America, PCA, Defendant Fawn Weaver, and Defendant Keith Weaver SHALL each file either (i) a notice of no objections to the proposed appraisers or (ii) written objections to the qualifications and/or disinterestedness of one or more of the proposed appraisers.”

My Pacer Budget hates this for me.

“After reviewing these filings, the Court will promptly appoint three appraisers (or order the Receiver to propose additional candidates if appropriate) and enter other orders as necessary t facilitate the completion of 28 U.S.C. § 2001(b)’s pre-sale requirements. This will culminate in a properly noticed hearing regarding whether the Court should approve the proposed sale of the Martha’s Vineyard Property.

SO ORDERED.”

Notably, this order doesn’t invalidate the receivers ability to make the sale, it sets out a very clear roadmap of HOW to sell it.

My favorite thing about this is that The Weaver (TM) did not at any time make this argument. The Judge essentially did the work for them. Not because the judge is crooked, but because the judge must follow existing law. Whatever appeals may come of this case, this order will have been bulletproof.

Is this a W for the Weavers? If a delay is the goal, then yes. This pushes things back at least another month.

I believe this actually to be another Big Fat L for them, mainly because this now opens those “offers” up to competitive bids, and delays their ability to back door getting that house back.

Waiting for the judge to rule is like watching paint dry.

UPDATE 3/14-

As we all wait for the judge to rule, and brace ourselves for another insufferable episode of Sunday With The Deceivers (TM), there is quite a bit going on behind the scenes. I can’t quite tell you all about it yet, mainly because weekends are for touching grass, and also because as soon as I do a big post, the judge will rule. So get outside, and have a beer. I’ll be back Monday, hopefully with the judge and his irk stick.

It’s Farm Credit’s money and they want it NOWWWWWWWW!

UPDATE 3/11-

Got a quick one for you today (I hope). Farm Credit had a brief filing in support of the sale of the Martha’s Vineyard house. No cold brew for me today, it’s Easy Like Sunday Morning.

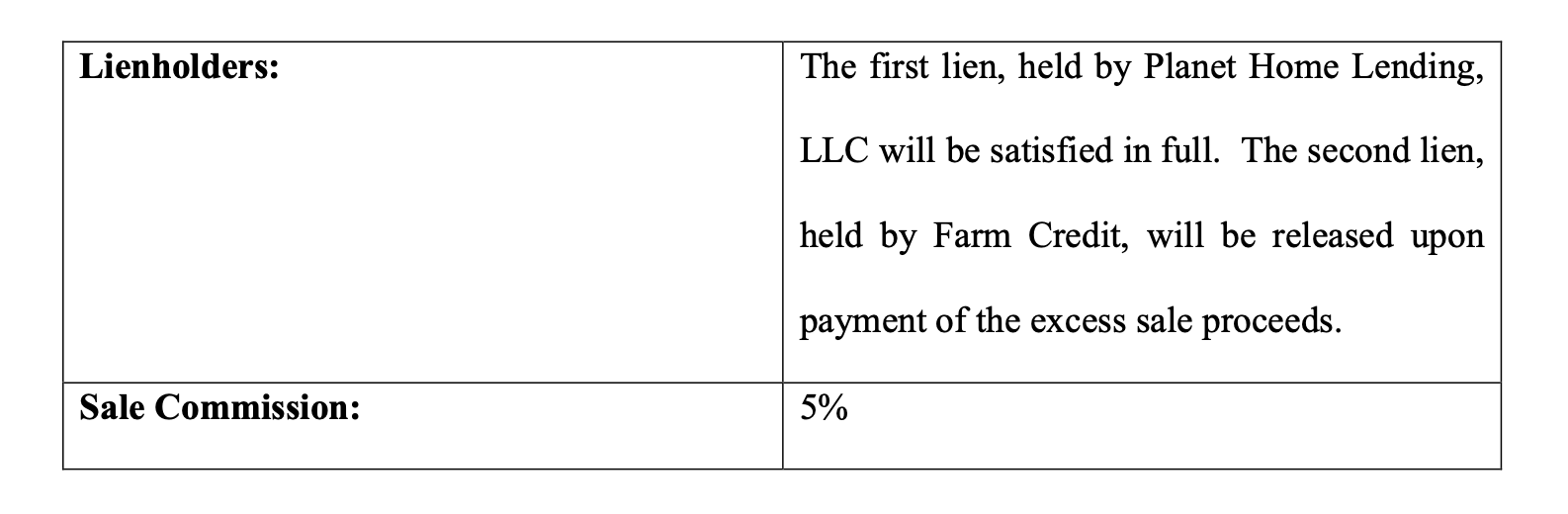

“FCMA has a lien on the net cash proceeds of the sale of the Martha’s Vineyard property (the “MV Property”)5 because the MV Property was purchased from proceeds of the FCMA Loans. The fact that FCMA loaned $2,300,000 to Uncle Nearest to purchase the MV Property is undisputed. Accordingly, the net cash proceeds of the sale of the MV Property are subject to FCMA’s liens.”

Imagine the bank, via billable hours no less, having to spell this out. They loaned money to Uncle Nearest Keith. Who then bought a house for UN MV HOUSE Keith, who then mortgaged that house to a different bank, and then did who knows what with that money, and now The Weaver (TM) saying she doesn’t want the bank to see the proceeds of the sale, even though she’s probably quietly (for once) backing the offers on that house to begin with.

Did you know that basketball player Kevin Johnson’s “offer” is via Nubian. Did you know that Nubian is a series C investor in Uncle Nearest?

The bank then goes over the background of the loan and loan terms, which has already been filed in previous documents to the court. No need to waste finger energy on it this morning as there’s nothing new here.

Bank loaned money, knew what the loan was for, was surprised that the collateral was moved etc..

“Although FCMA was aware that Uncle Nearest was acquiring the MV Property, it did not anticipate that Uncle Nearest would transfer the property in violation of the Credit Agreement. In Amendment No. 4, FCMA loaned money to Uncle Nearest for the sole purpose of purchasing the MV Property. Additionally, as set forth in FCMA’s Verified Complaint, Uncle Nearest did not purchase the property in its name. Instead, it used an undisclosed new entity (UN House MV) to take title to it and then, Uncle Nearest subsequently mortgaged it to another lender.”

“In further violation of Amendment No. 4 and the Credit Agreement, Uncle Nearest did not inform FCMA that Uncle Nearest had not designed the transaction to issue title of the MV Property to Uncle Nearest.”

Investors were told in emails that the house was “pledged” to Uncle Nearest. Whatever that means. I pledge that I will pay money for services rendered by small businesses, and then don’t pay them. Pledges from The Weaver (TM) are about as legitimate as a bag full of $6 bills.

“Despite Ms. Weaver’s statement that “[t]he transaction and all relevant details regarding the same were timely disclosed to Farm Credit,”10 FCMA only learned what actually happened through its own investigation and through no disclosure from Uncle Nearest.”

The Weaver (TM) likely thought she’d bamboozled the bank, not knowing that the bank was already looking into things. The question that arises from this, is how long did the bank know that shenanigans were afoot? And if it was a long time, did they report said shenanigans to any regulatory agencies? Failure to do so would be serious stuff indeed, but wouldn’t change any of the facts in this civil case.

“Even if the funds were moved via a loan from Uncle Nearest to UN House MV in violation of the Credit Agreement, then such loan is nonetheless an asset of Uncle Nearest and is therefore FCMA’s Collateral.”

The bank- We don’t care how you moved the money, that house is ours.

“The Weaver Parties make much of the fact that FCMA did not require a mortgage on the property. It is not uncommon for lenders to forego a contractual lien on a borrower’s property when the lender has the benefit of a “negative pledge” covenant like the one found in Section 7.1 of the Credit Agreement. Such a covenant prohibits the granting of liens on borrower property unless expressly permitted by the Credit Agreement. Additionally, providing a freely assignable purchase contract in Mr. Weaver’s name prior to Amendment No. 4 does not demonstrate that FCMA knew the property would be titled in the name of UN MV House. Indeed, an assignment of that contract was necessary for Uncle Nearest to comply with the terms of Amendment No. 4.”

The bank- Stop playing, that money is ours.

“As the Receiver correctly stated, FCMA has an interest in the proposed $900,000 in sale proceeds. The relationship between UN MV House and Uncle Nearest is unclear, but the fact that FCMA has a claim with respect to the proceeds of the sale of the MV Property is undisputed.”

The bank- Again, we don’t care how you did what you did or why, that’s our money.

“FCMA has a lien on substantially all of Uncle Nearest’s assets, including a lien on cash. Therefore, any amounts to which Uncle Nearest is entitled from the sale of the MV Propertyare proceeds of FCMA’s Collateral.”

The bank said early on that all assets of UN were encumbered in some way, essentially every asset was collateral for some debt.

The bank just said, sell the damn thing and give us our scratch.

This really is the worst puppet show ever.

UPDATE 3/10-

We had a brief respite now didn’t we? Cap’N Phillip dropped a 5 page filed response regarding the Martha’s Vineyard House. I’m trying a new Cold Brew this week (my local was out of my preferred French Truck), so wish me luck.

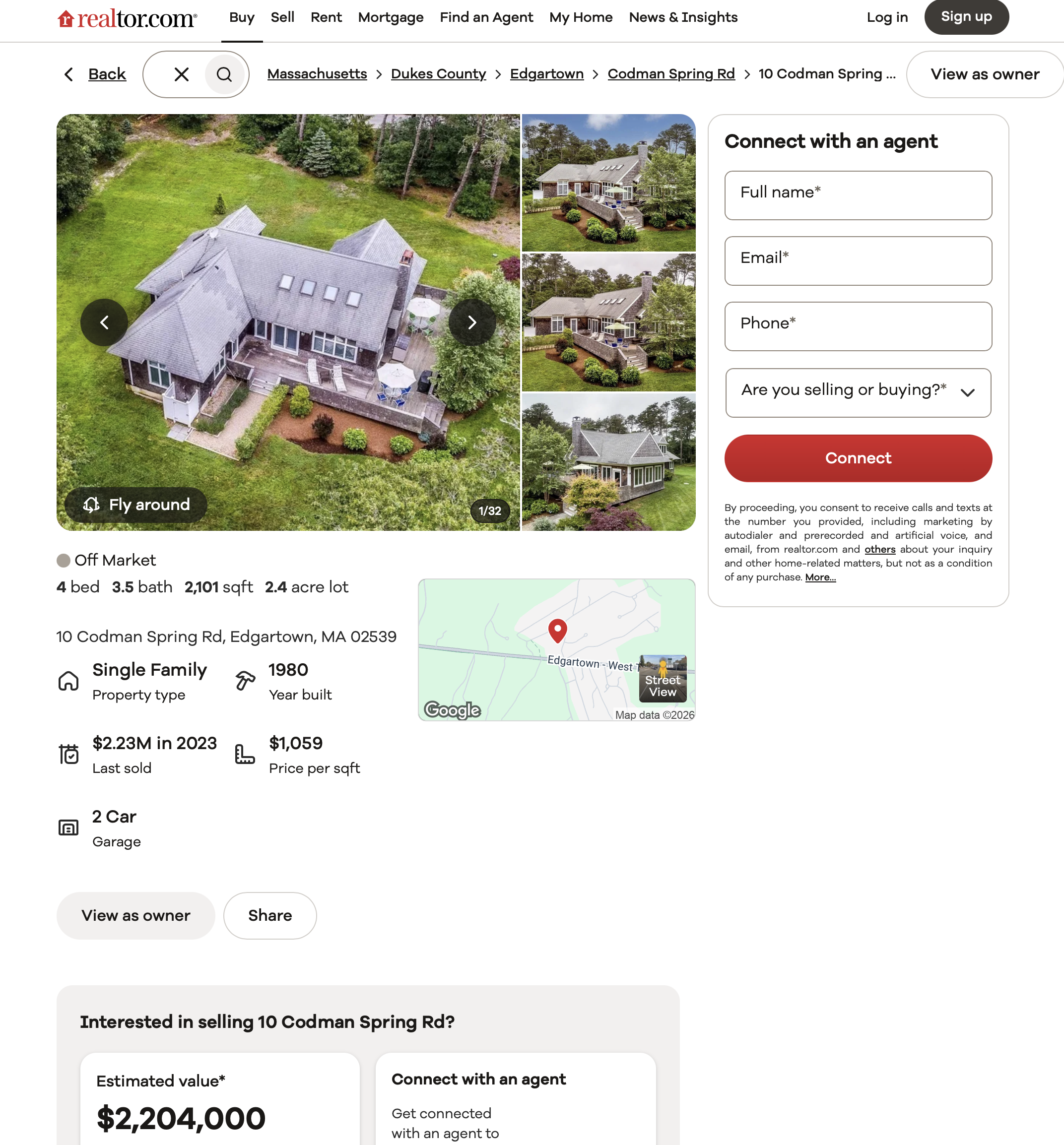

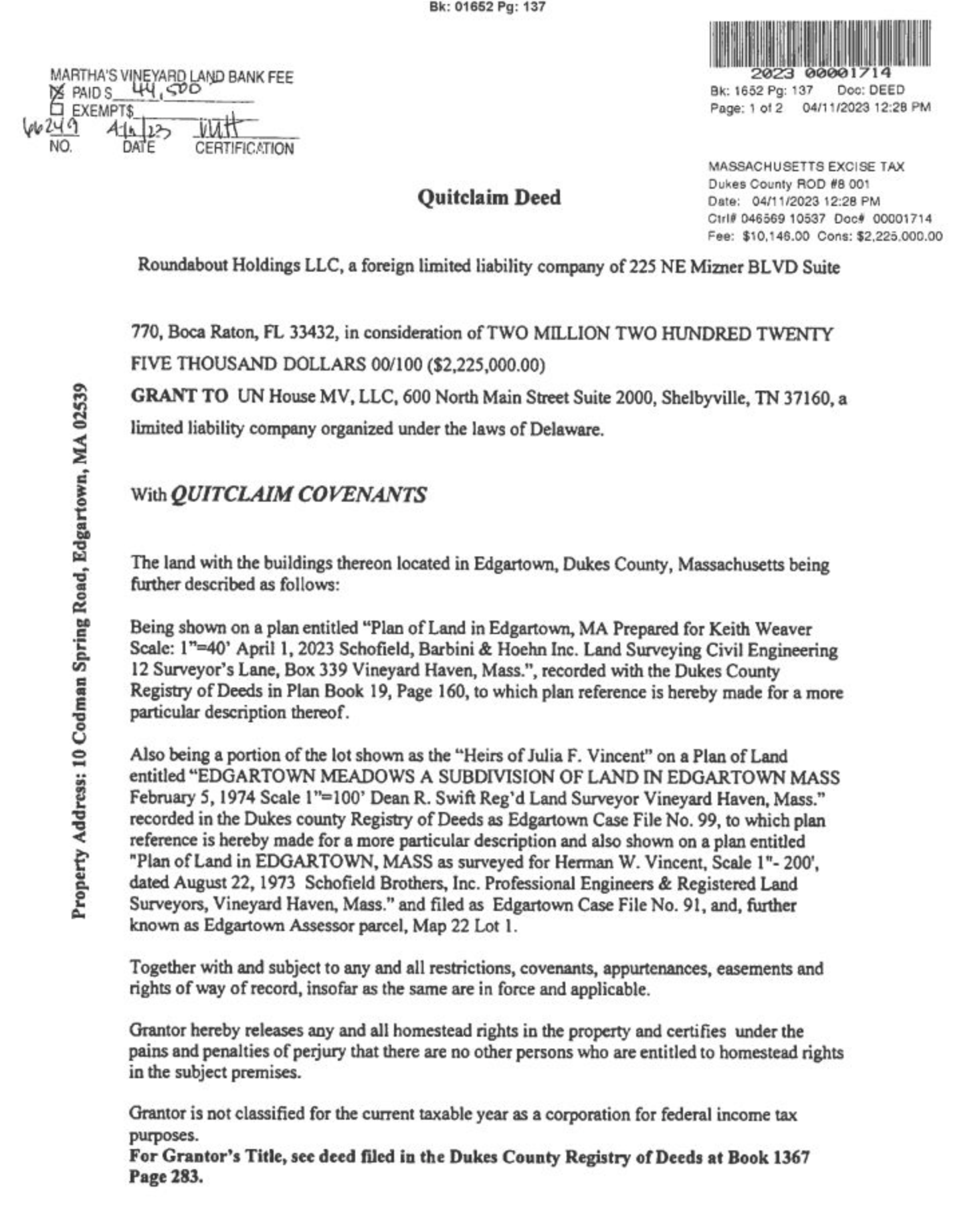

“In their opposition to the relief sought by the Receiver in the Motion, the Weaver Parties raise four objections to the proposed sale: (1) the sale is premature, as the Court is considering a motion to essentially terminate these proceedings; (2) a sale of the property located at 10 Codman Spring Road, Edgartown, Massachusetts (the “Martha’s Vineyard Property”) would damage the “enterprise value” of Uncle Nearest, Inc.; (3) the sale proceeds should not be distributed to Farm Credit Mid-America, PCA (“Farm Credit”); and (4) the Weaver Parties promised that another offer would be forthcoming that would provide the receivership estate with the “same economic benefit.” The Receiver will address each of these objections in turn. However, it is first important to note what the Weaver Parties do not contest. The Weaver Parties never argue that the proposed sale price is insufficient. They never argue that the sale process was commercially unreasonable. They never argue that the proposed buyer is an insider or somehow otherwise a disqualified purchaser. These missing objections are significant as it signals to this Court their admission that both the process and the result of this proposed sale is acceptable.”

That The Weaver (TM) has offered up such a weak opposition to this sale definitely has my attention.

“Turning to the objections raised to the proposed sale in the Weaver Parties’ Response, they first contend that the Motion is premature, as the Court is still considering their Motion to Reconsider, which would terminate this receivership. This would be a valid concern but for the timing of the Motion. The Court has already conducted a seven (7) hour hearing on the Motion to Reconsider and the briefing on that issue is closed. The Receiver trusts that the Court would not grant this Motion unless and until it was certain that it has no intention on terminating these proceedings. Therefore, this concern is moot due to the status and timing of these proceedings.”

Ah, remember the old “denied as moot?” I can’t wait to see what gems the Judge drops on us in his orders.

“Second, the Weaver Parties object to the proposed sale because a sale of this property would negatively impact the “enterprise value” of Uncle Nearest. The Weaver Parties admit that the only value of the Martha’s Vineyard Property is for marketing and advertising purposes, and they concede that otherwise it is a monthly cash drain on this receivership estate. Their argument, then rests upon the premise that this property is somehow important to the financial rehabilitation of the Company. The Receiver disagrees. “

It’s hard to impact a negative enterprise value. Selling this house, that the neighbors loathe, is a good move for the receivership, and will not harm this shell of a brand.

“As he has made clear to the Court and to all of the parties, the Receiver believes that the only path forward for this Company is the sale of its assets to a third party. In that regard, he consulted with Arlington Capital, his investment banking consultant, about whether to include the Martha’s Vineyard Property as part of the Uncle Nearest portfolio or whether it was wiser to sell it separately. Since this property was not income producing, not geographically related to Uncle Nearest’s operations, and not historically tied to Uncle Nearest’s origins, Arlington Capital suggested that the Receiver attempt to sell this property separately. They offered the same advice regarding the assets located in Cognac, France and the assets related to Square One Vodka. Indeed, none of the potential purchasers of the business assets have inquired about purchasing the Martha’s Vineyard Property, which is well known to be affiliated with Uncle Nearest. Therefore, the advice of professionals and the marketplace have confirmed that the Martha’s Vineyard Property is not critical to the “enterprise value” of Uncle Nearest; it should be sold separately.”

No one wants a house that is a money pit on their books unless they’re rich enough to live in it.

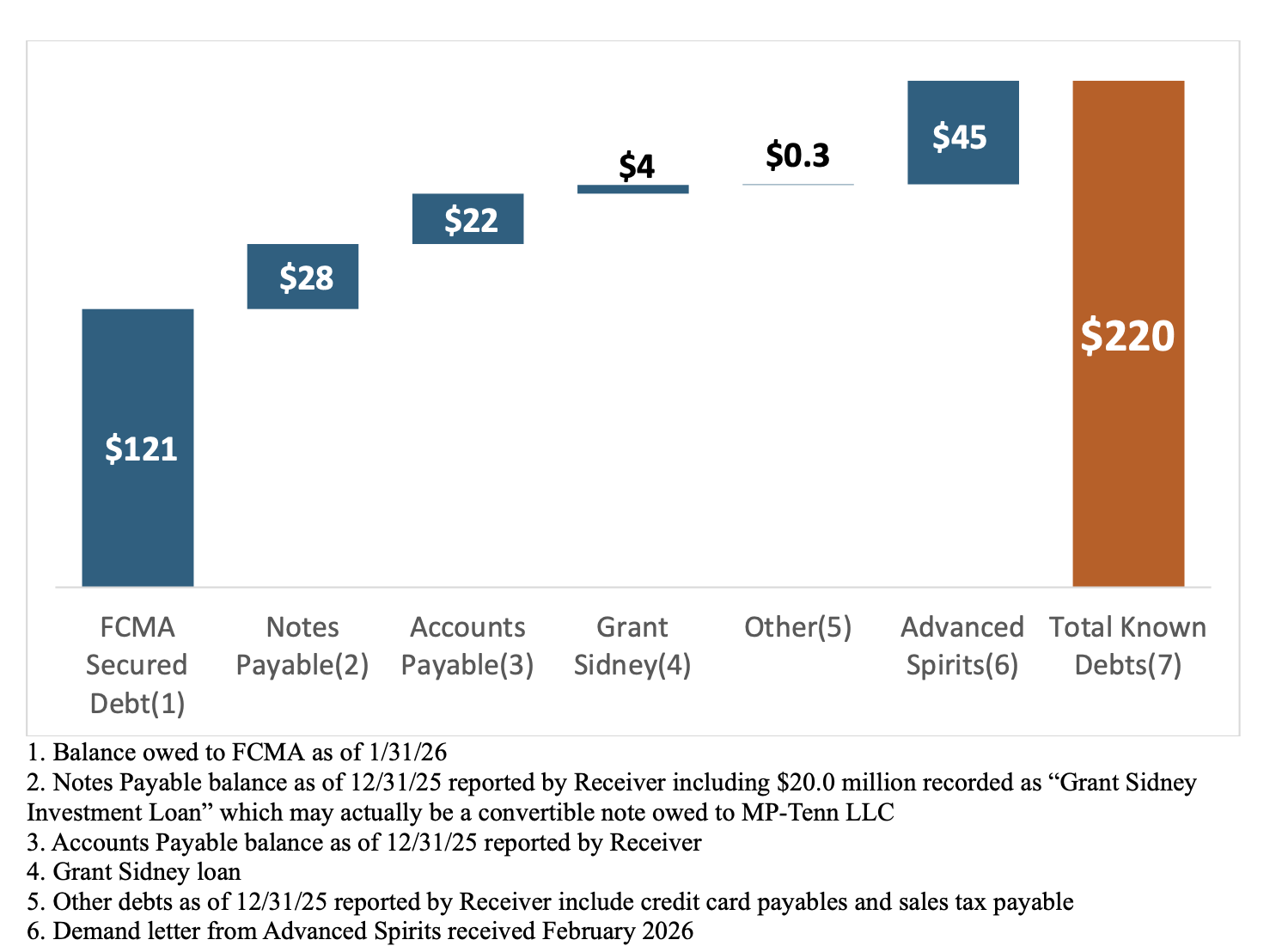

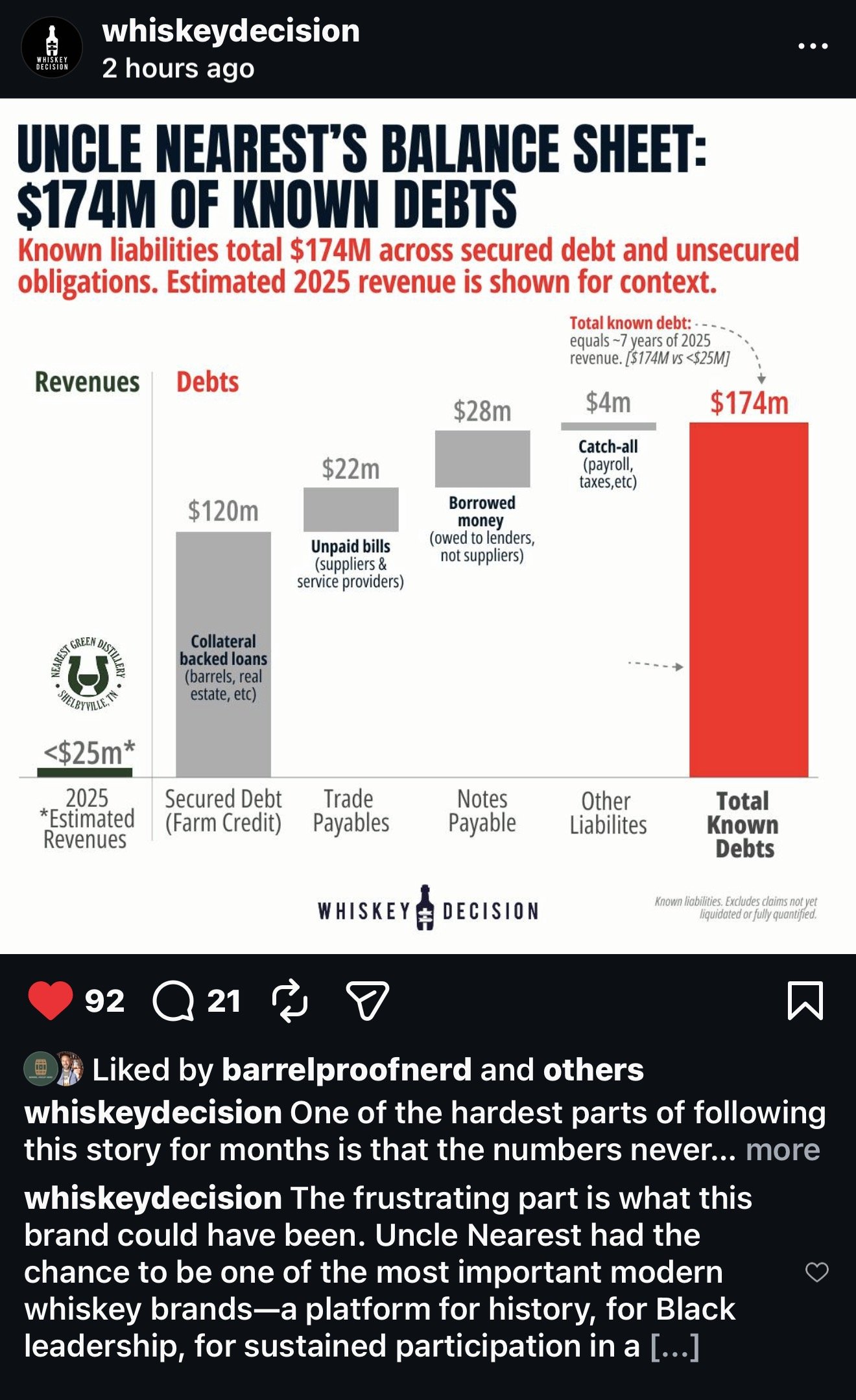

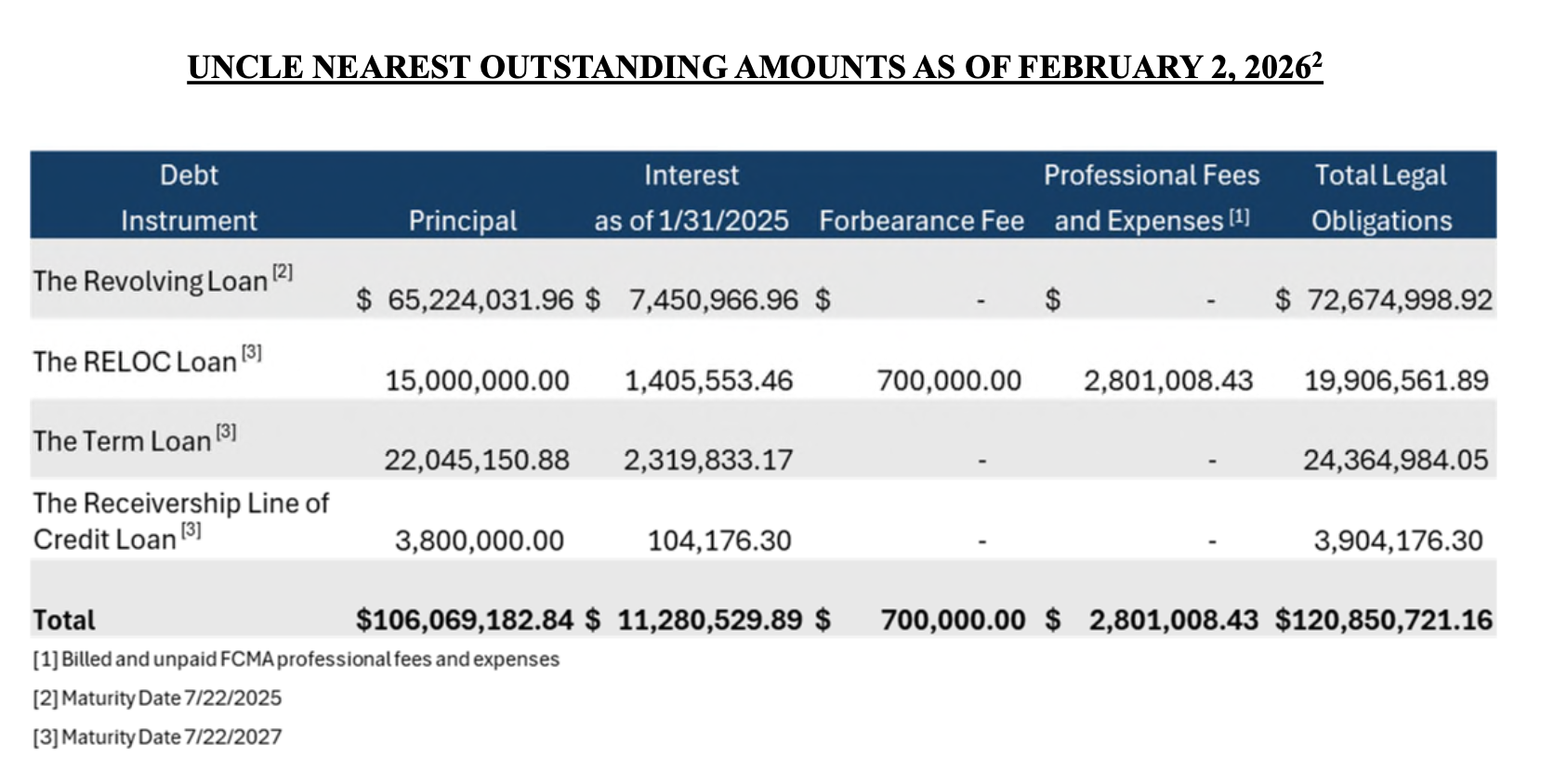

“Third, the Weaver Parties contend that, even if the property is sold, its proceeds should not be distributed to Farm Credit. This argument is particularly perplexing as the Weaver Parties have admitted throughout these proceedings that the Martha’s Vineyard Property was directly purchased using the proceeds from Farm Credit’s loans. For example, as recently as February 5, 2026, the Weaver Parties acknowledged that Farm Credit knew that they were purchasing the Martha’s Vineyard Property with their loan proceeds, and knew that it was being purchased by Keith Weaver, not by Uncle Nearest. The Receiver believes that this Court would expect him to use the proceeds from this sale to pay down the Farm Credit debt, which is now approaching $120 million.2 If the Court disagrees, it could always order the funds to be interpleaded or order the Receiver to hold the funds in escrow, pending the outcome of this matter.”

I feel that the idea of giving the bank one nickel of the money owed to the bank at this point is so galling to the Weaver’s, that they keep making stupid arguments.

“Practically, it matters little. This receivership estate has depended upon, and will continue to depend upon, further advances by Farm Credit to operate the business. Whether the Receiver tenders the $900,000 net proceeds to Farm Credit, which in turn loans it to this receivership estate – or whether the Receiver retains the $900,000 thereby reducing future loan advances from Farm Credit – creates the same result for the estate.”

That’s what insolvency is. Needing other peoples money to pay the bills. The Weaver (TM) couldn’t run any of the related businesses without the continuous infusion of money into those businesses via fees charged among entities that were owned and controlled by the same people.

Sunday with the Deceivers (TM) needs a reboot.

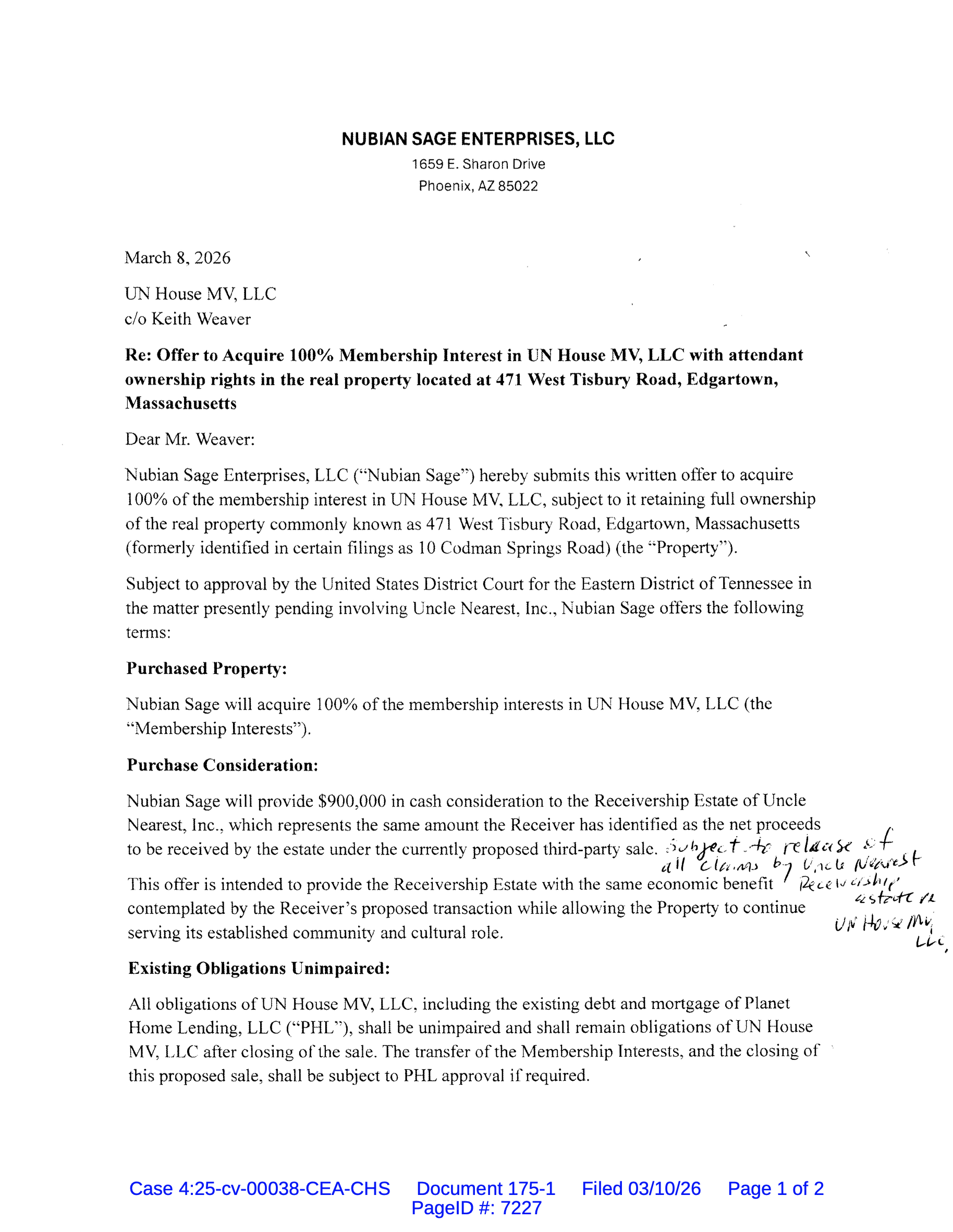

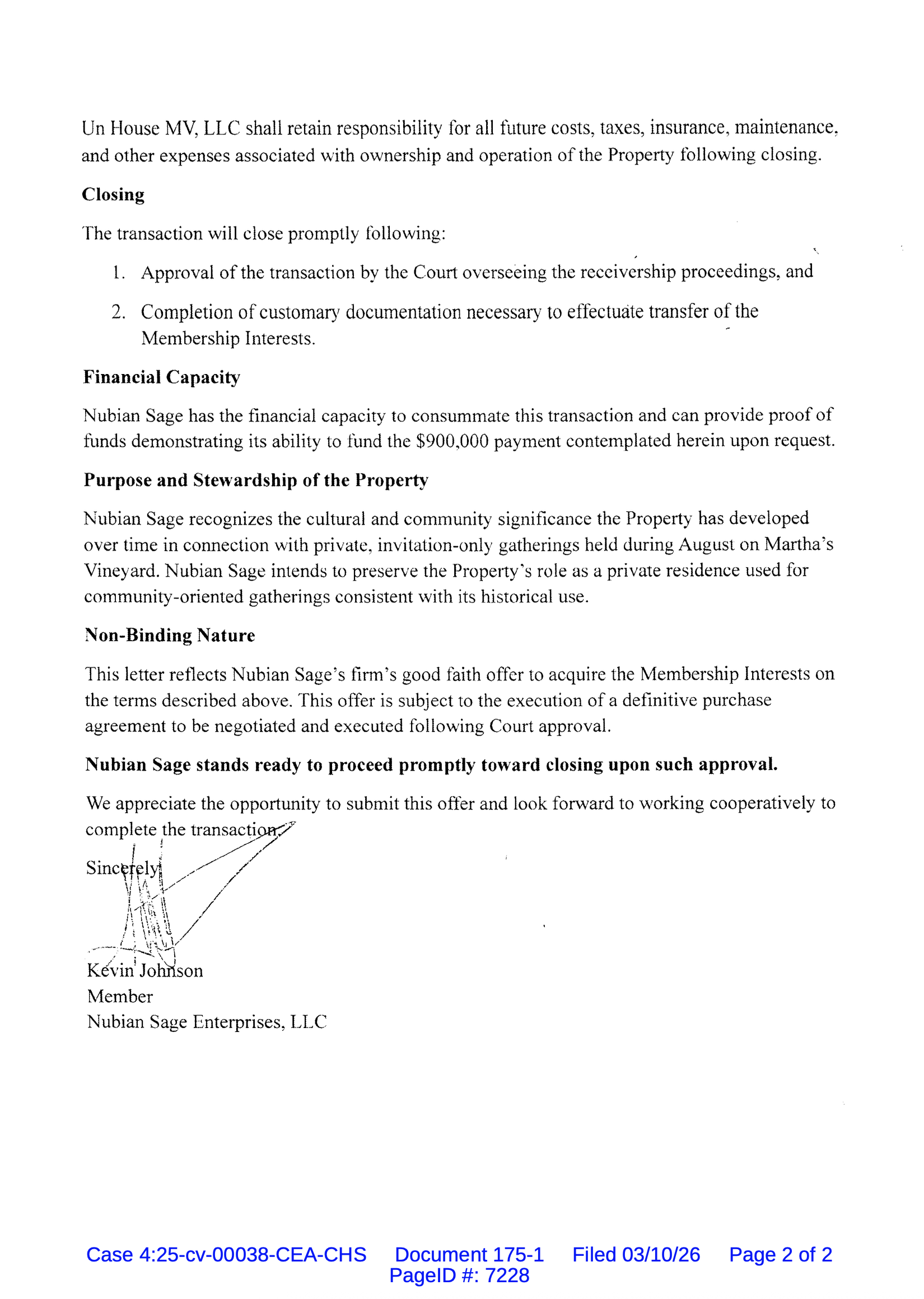

“Finally, the Weaver Parties ask the Court to reject the offer to purchase the Martha’s Vineyard Property proposed in the Motion, even though it is set to close in a matter of days, in favor of a non-binding offer to acquire 100% of the membership interest of UN House MV, LLC made by Nubian Sage Enterprises, LLC (“Nubian”). A copy of this non-binding offer letter is attached hereto as Exhibit A. 3 Upon information and belief, Nubian is an investment company owned and operated by Kevin Johnson. The Receiver had conversations with Mr. Johnson prior to accepting the offer that is now before this Court. The Receiver believes that Mr. Johnson has the ability to purchase the Martha’s Vineyard Property and likely has legitimate interest in it. The Receiver had at least two conversations with Mr. Johnson a week or more prior to accepting the current offer, and sent him information concerning the costs and expenses associated with maintaining the property. “

Kevin Johnson is also well known to the Weavers. Cap’N turned him down.

“The Receiver even offered to meet Mr. Johnson in Martha’s Vineyard to show him the property and, if all appeared satisfactory, to sign a purchase and sale agreement with him. After that conversation, the Receiver did not hear back from Mr. Johnson until an email on March 2, 2026, approximately eleven days after the Receiver had already filed the present Motion, asking the Receiver to reach back out. Then, on March 9, 2026, counsel for the Weaver Parties emailed the Receiver an offer that was allegedly made by Mr. Johnson’s company.”

Two things here- Firstly, KJ doesn’t have the money. Secondly, note the last line- “an offer that was allegedly made by Mr. Johnson’s company.” By now we all know what this means don’t we? I don’t need to spell this out do I? Allegedly The Weaver (TM) is behind this.

“The Receiver has a number of concerns about the Nubian offer. First, the offer is non- binding on its face. Second, it is likely subject to approval and consent by Planet Home Lending, LLC (the mortgage holder), since the mortgage is being assumed as part of the Nubian offer. The Receiver has had no contact with Planet Home Lending, LLC and has no way of knowing (on such short notice) whether it would consent to the mortgage assumption. Third, a transfer of the membership interest of UN House MV, LLC is a substantially more complicated transaction than a simple real estate sale, as currently contemplated. The Nubian transaction would cost the estate additional attorney fees to consummate.”

I had a number of concerns when three allegedly unrelated to The Weaver (TM) parties, made essentially identical offers on the same property. These three offers are likely meant to confuse, delay, and derail.

“The offer was transmitted to the Receiver and his counsel by Michael Collins after hours on March 9, 2026, so the Receiver has had no opportunity to vet the offer.”

Doubtful Michael Collins was up late filing things without the puppet master making him do so.

“Fourth, despite having prior, direct contact with the Receiver by email, Nubian purportedly directed its offer to Keith Weaver, whose counsel then relayed it to the Receiver and his counsel. The Receiver has had no opportunity to confirm the authenticity of the Nubian offer. Finally, the Nubian offer is not a higher and better offer than the one that is already before the Court for approval; at best, it is an equivalent offer. For all of these reasons, it is the Receiver’s business judgment that the offer presented for approval in the Motion is the superior offer.”

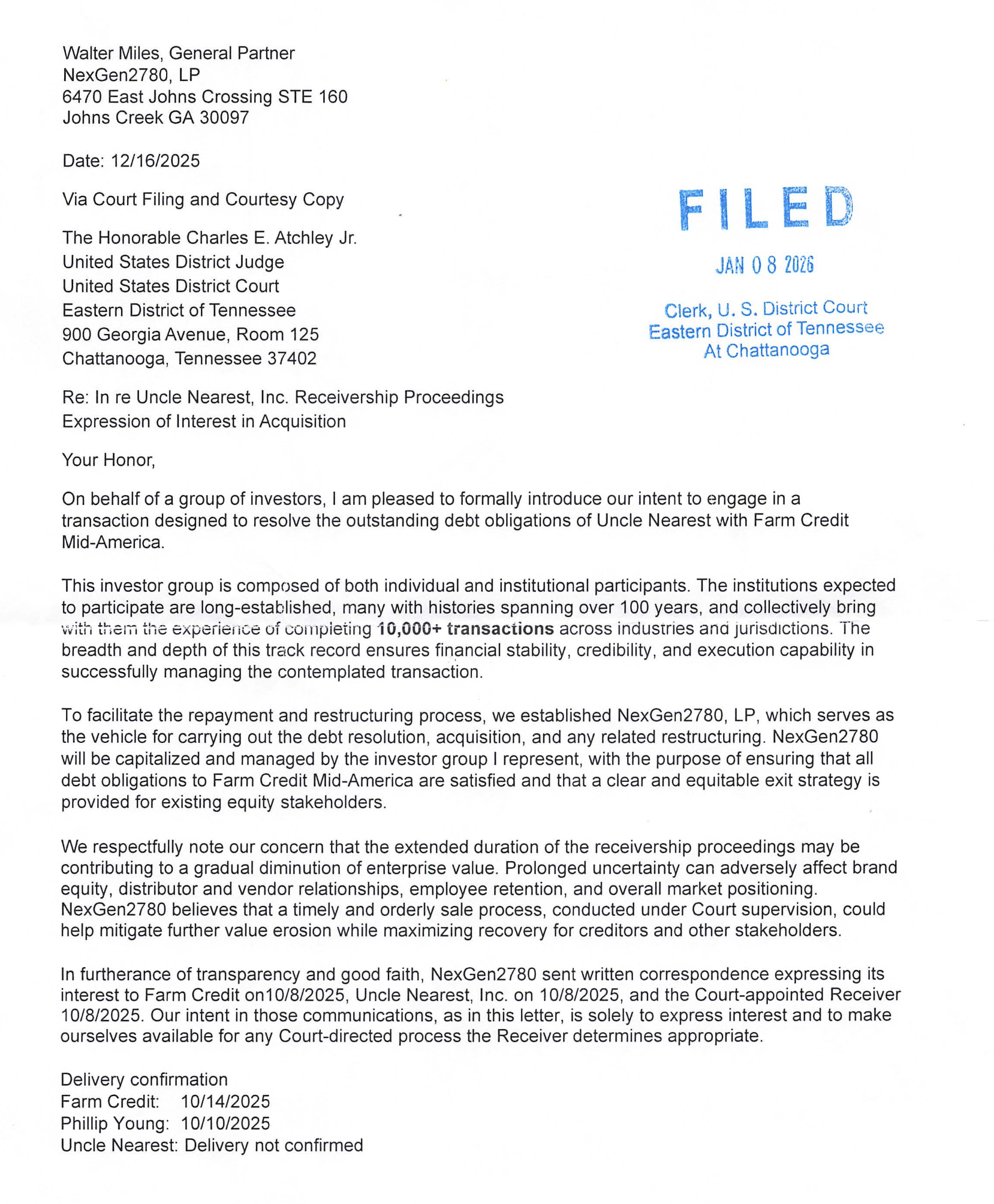

I mean, this is all seemingly so familiar. NexGen part two anyone? Will we get an offer mailed directly to the court next?

“The Receiver believes that the record before this Court supports his decision to sell the Martha’s Vineyard Property, and there has been no objection to the sale process, the sale amount, or the proposed buyers. WHEREFORE, the Receiver request that the Court grant his Motion.”

Cap’N Phillip was polite about the offers. I’ll give him that. I’ll include the offer letter exhibit in the images below.

Subject to release, hand scribbled. Spidey senses are tingling.

Non-Binding. KJ knows there are other offers. This is unserious?

Wait, what did he say yesterday? A board member of UN hired a high powered and expensive law firm?

UPDATE 3/8-

With so much going on everywhere all at once, I truly lacked the desire to get into The Weaver (TM) filings, but I know that I have to. So, let’s get to it. Remember, these are all highly repetitive, so even though each of the Seventies (TM) filed individually (they are required to), they used the same CatGPT. For the sake of brevity, I won’t be dissecting the redundancies. Got your Sunday with the Deceivers (TM) cold brew ready?

QUILL AND CASK OPPOSING INCLUSION

“The burden of proof on the issue of whether the Non-Parties, including Q&C, should be placed in Receivership is clearly on the Receiver and Farm Credit and the burden is high. The Sixth Circuit has recognized that placing a company in receivership is an extreme form of relief justified in very limited circumstances. Those circumstances are clearly not present in this case and the Motion to Clarify never should have been filed prior to any investigation by the Receiver.”

This is true. Receivership is rare, and difficult to order by a court. It’s a drastic, last ditch measure to protect assets and secure debt repayments by any means necessary. That Uncle Nearest was placed in one tells you how seriously bad things were over there. Frankly, even if Farm Credit hadn’t filed this suit, Uncle Nearest was in severe debt, and hadn’t been paying its bills for quite some time. The bank loan default wasn’t an anomaly, it was a foundational feature of How the Weaver’s ran their businesses. Alleging that Cap’N Phillip didn’t investigate before asking for inclusion, begs the reader to be be as dumb as a box of Pet Rocks (Yeah, I still have mine).

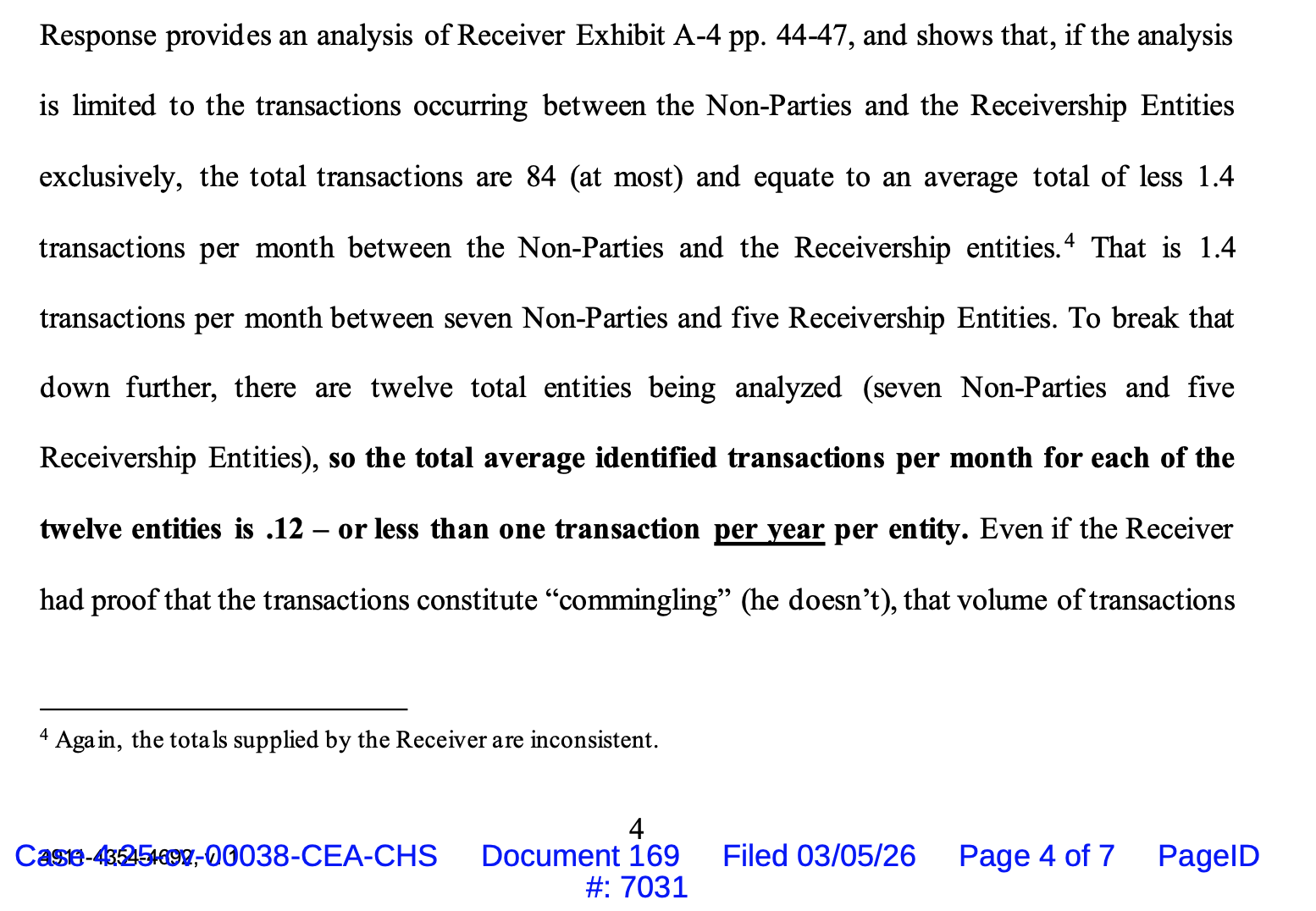

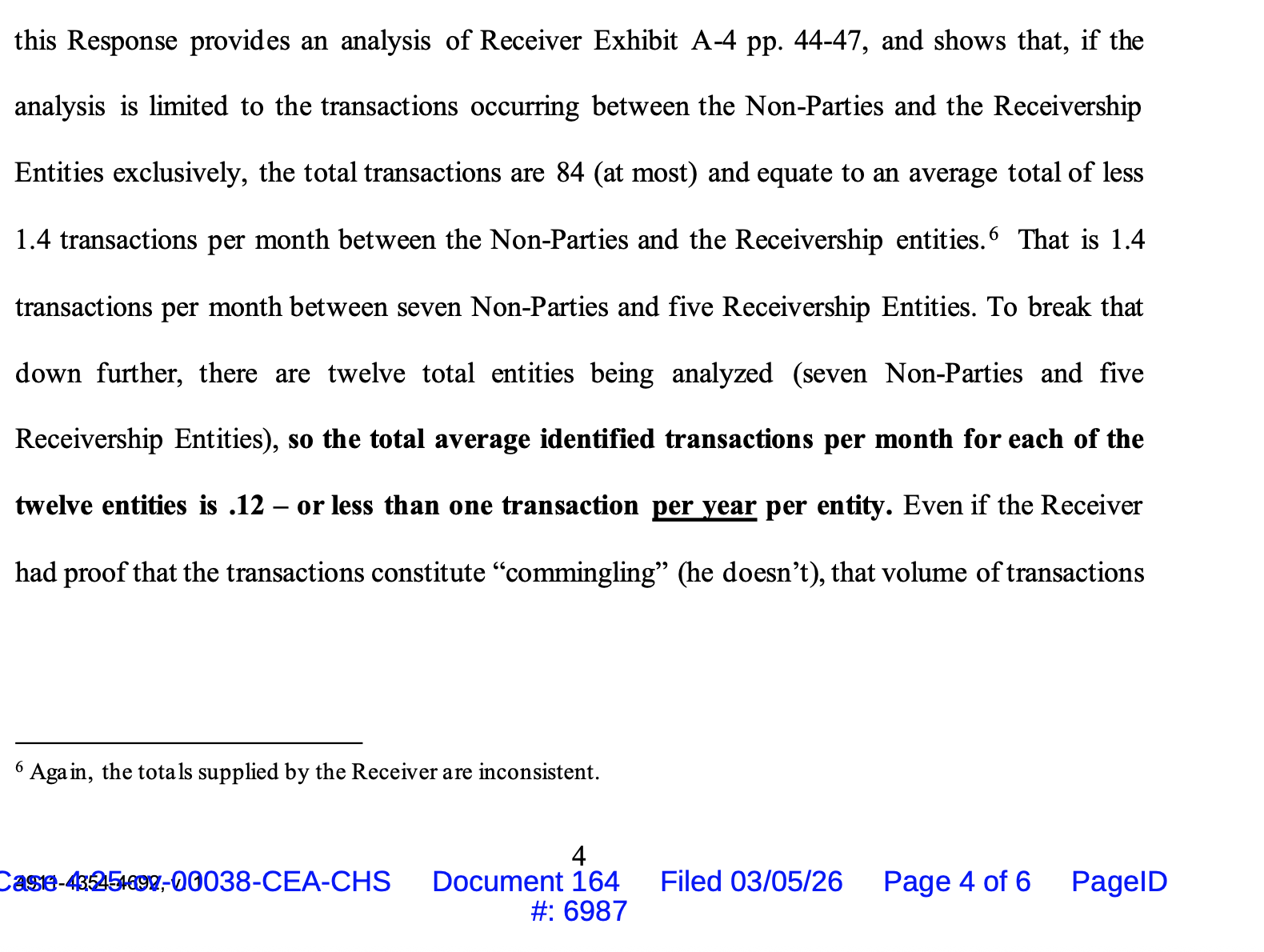

They then spend some billable paragraphs on trying to redefine what commingling means. It’s dull, and ineffective. They also try to equate the “shared employees” thing with the no-employees of Quill and Cask and thus render the inclusion request improper. It was a general statement by the Receiver in his filing, but wasn’t directed specifically at Q&C. Q&C doesn’t really address the reasons the receiver provided for inclusion (like the equity investments of $800k, which conflicted with Keith’s claim that he didn’t own any stake in UN) and focuses on a more general defense of “there were not that many transactions.” Expect more of the nonsensical semantics as we go through the rest of the Seventies (TM).

I really am enjoying the weird spacing on the footnote.

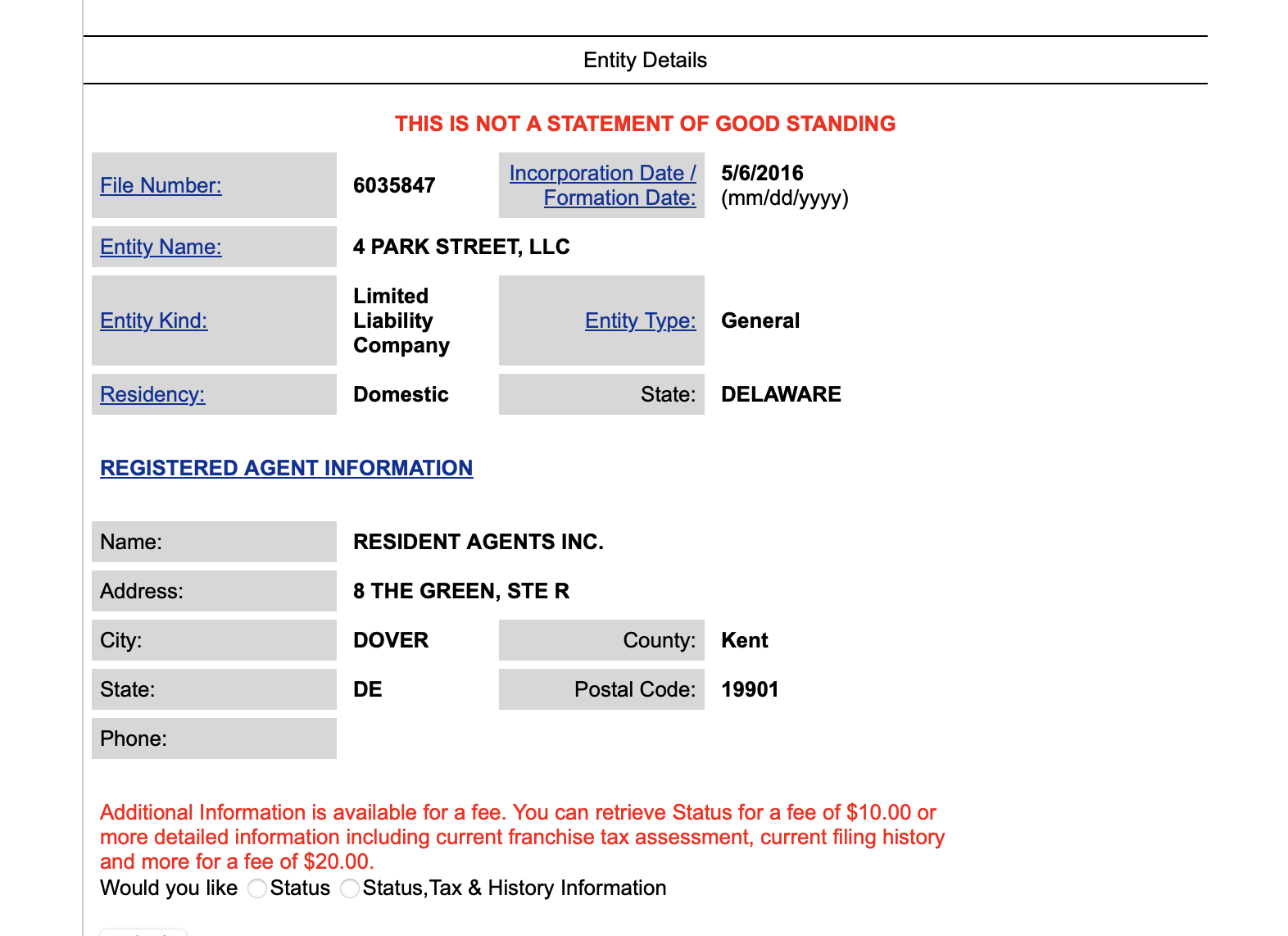

Next up, 4 Front Street LLC.

They do the redefine commingling thing, no shared employees, copy and pasted, only the LLC has changed.

There is nothing new to include here from 4 Front Street LLC, and just for the giggles, and to prove that it’s copy pasted…..

Different filing, same text, including the footnote goof.

Let’s do some BBQ now.

Receivership bad, not warranted, redefined commingling, no shared employees, copy paste….

“SBH pays Mr. Baker a 6% royalty fee for the use of the Chuck’s Barrel House BBQ brand and operating system. Mr. Baker also provides the proprietary sauces and rubs used by the restaurant on a consignment basis, which are later paid for by SBH in the ordinary course of business. SBH also repays Mr. Baker for his investment of approximately $300,000 for the kitchen and related equipment, which SBH has been systematically repaying over time. None of these expenses have been paid by any of the Uncle Nearest Entities, and there is no assertion any the Receiver otherwise.”

Note the use of the phrase “repaying over time.” aka, UNPAID DEBT. Please also note that the bolded typo in the document is in fact their typo, and not the result of any fat fingered goof on my part. Also, prior to opening, money came in from UN for operational start up costs, and likely continued after.

“There are absolutely no employees shared between Uncle Nearest and SBH – none. There is no evidence in the record of any sharing of employees.”

This might be true, technically, but probably is not. HB and SBH have definitely shared employees, and are currently doing so with Humber Baron GM French Rankin asking guests if they want fries with that.

“As to the payment of rent, SBH asserts that any rent due is offset by the unpaid obligations owed by Uncle Nearest to SBH. Regardless, if the Receiver believes it is in the best interests of the Receivership Estate to terminate the Lease based on alleged non-payment of rent, then he has an adequate legal remedy to accomplish that. If he believes that SBH owes money to Uncle Nearest, he has an adequate legal remedy for that. Receivership is not the answer where there are clearly other, less invasive avenues to address the issues alleged by the Receiver.”

A business Keith owns, claims he doesn’t have to pay rent to a business he manages, and has an ownership stake in from another business he owns, because the business he manages owes a business he owns, money. Instead of receivership, he’s essentially saying sue the business I own, via the one I have an ownership stake in. People, if you’re confused, that’s the entire point.

This exhibit was filed by each entity.

Humble Baron now.

Receivership bad, not warranted, redefined commingling, no shared employees, copy paste….

“Second, the Receiver cites to the payment made by Uncle Nearest to Levy Foodservice as evidence of commingling when, in fact, the funds paid by Uncle Nearest to Levy were never mixed with Humble Baron’s funds.”

This is technically true. Mostly because UN paid for it, and HB did not. Semantical nonsense.

“Furthermore, the payment by Uncle Nearest to Levy has been shown to be in payment of Uncle Nearest’s own obligations, so it is not evidence of commingling or any improper or illegal act.”

Levy did sue Humble Baron. Uncle Nearest “paid it” (note, it’s still an unpaid debt). Interesting to note they included “illegal act” in there. No one said there was one.

“As to the payment of rent, Humble Baron asserts that any rent due is offset by the unpaid obligations owed by Uncle Nearest to Humble Baron. Regardless, if the Receiver believes it is in the best interests of the Receivership Estate to terminate the Lease based on alleged non-payment of rent, then he has an adequate legal remedy to accomplish that. If he believes that Humble Baron owes money to Uncle Nearest, he has an adequate legal remedy for that. Receivership is not the answer where there are clearly other, less invasive avenues to address the issues alleged by the Receiver.”

If this sounds familiar, that’s because it’s a copy/paste from the BBQ filing. Just the name change.

Defense donuts. When you got flavorless donuts, top them with wood chips and caviar.

Nashwood time.

Receivership bad, not warranted, redefined commingling, no shared employees, copy paste….

“Nashwood has provided certain event related services to the Uncle Nearest Entities over the years for the flat fee of $10,000 per month. That is not sharing of operational resources - that is providing operational resources for a fee, which is the very nature of operating a separate business.”

A business Keith owns, charges a business Keith manages and owns equity shares in via another company he owns, $10,000 a month for “certain services.” Which ones? Specifically which certain services?

Copy, meet paste. Typo be damned.

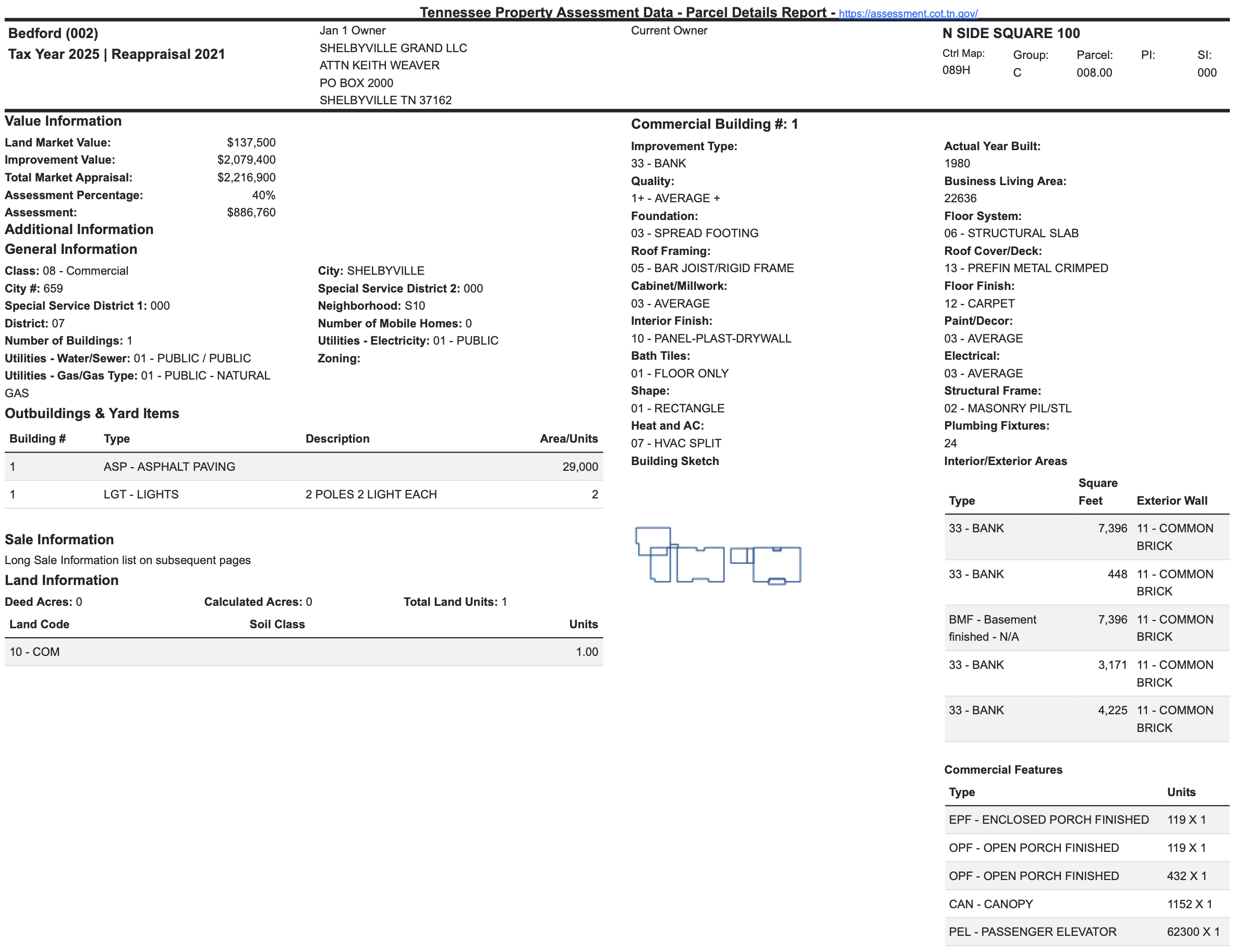

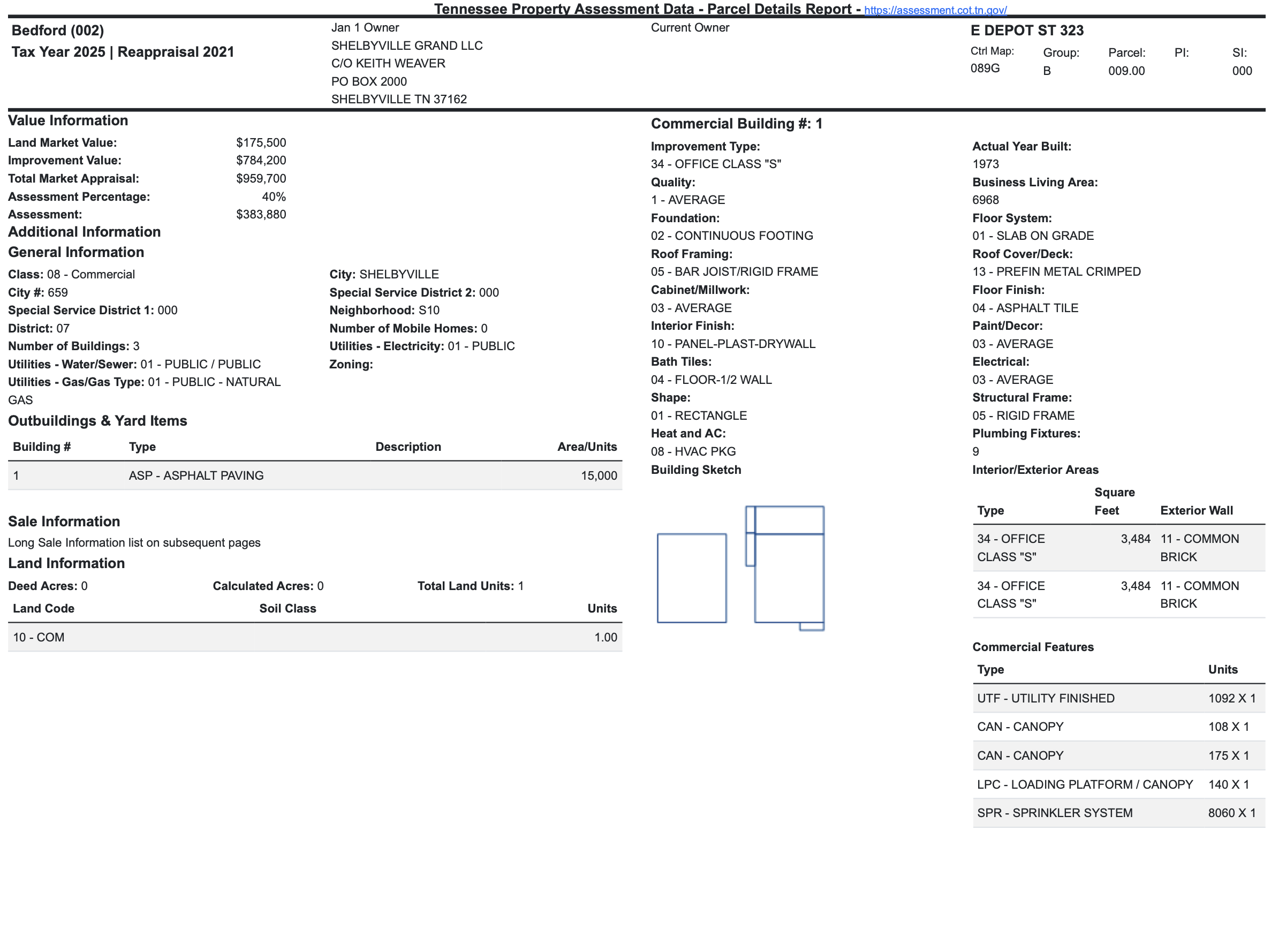

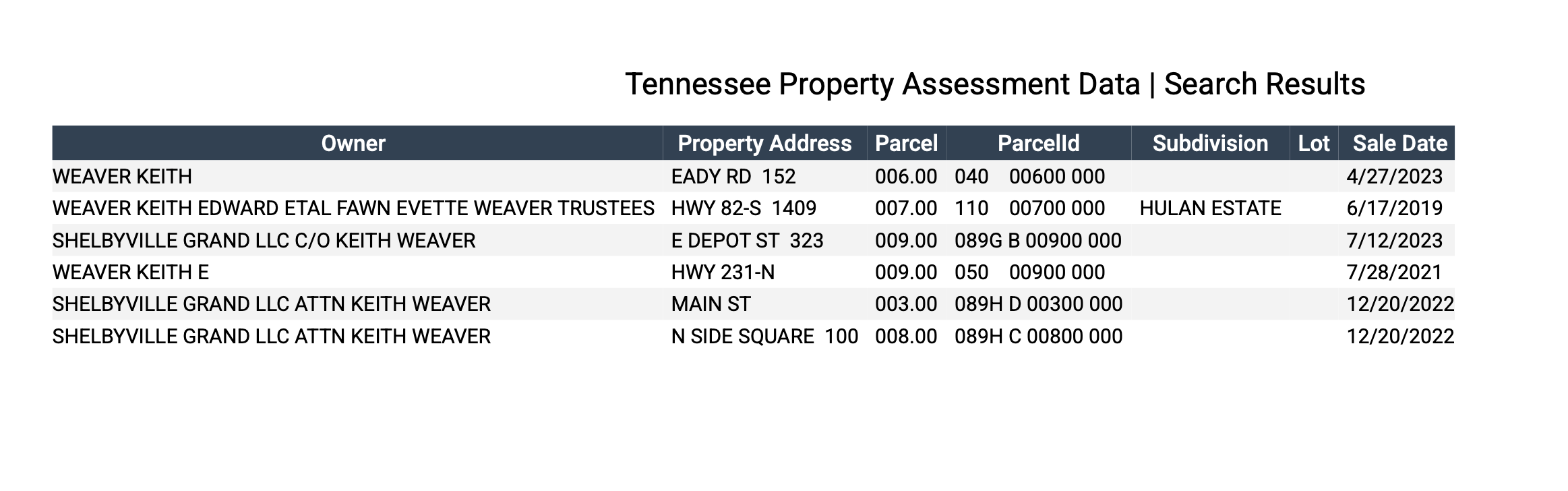

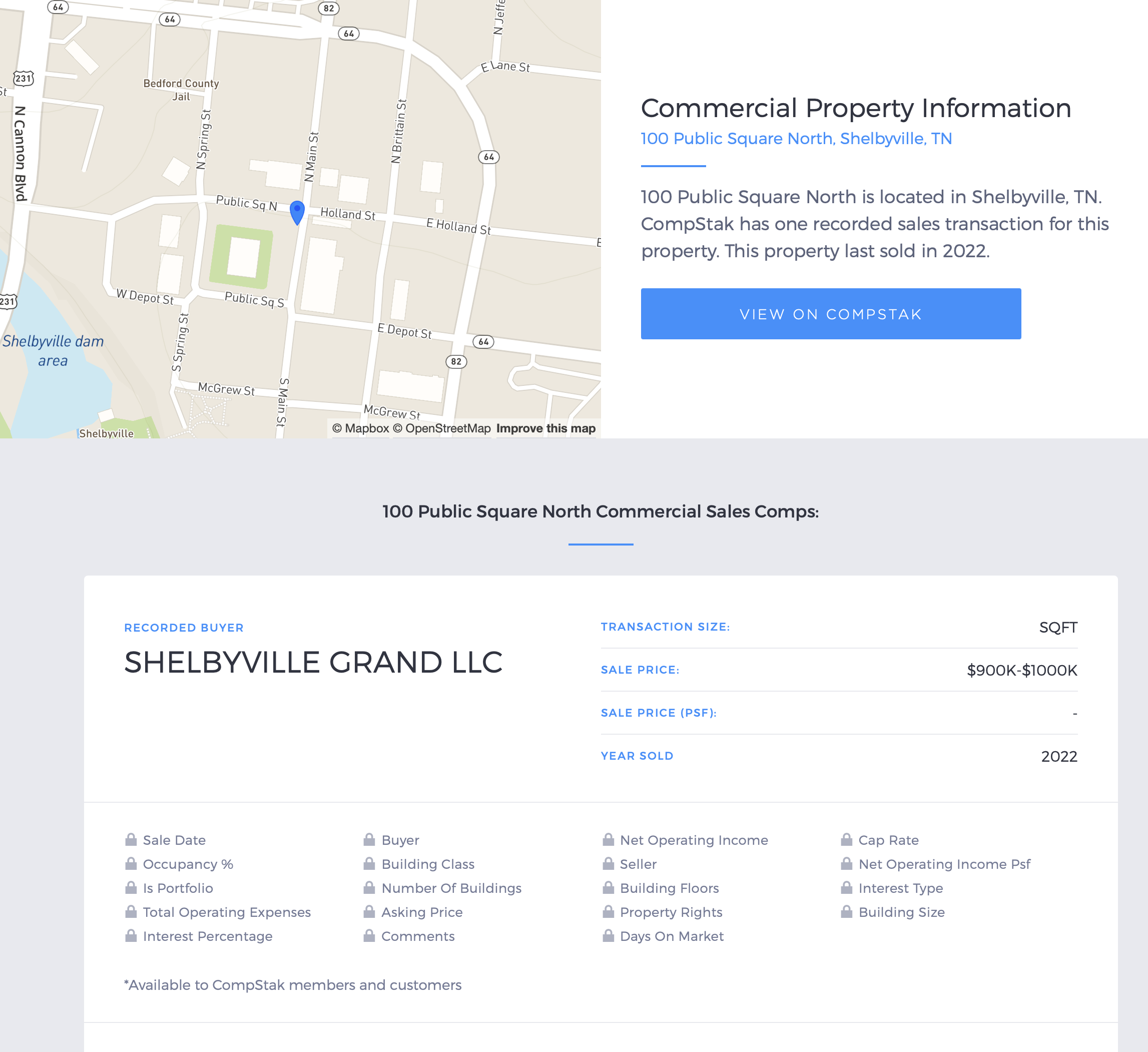

Shelbyville Grand.

Shall we check to see if there’s anything new?

Receivership bad, not warranted, redefined commingling, no shared employees, copy paste….

“The impact of the Motion to Clarify on SGLLC has been severe. The Receiver cites to a pending foreclosure action against one of SGLLC’s properties as support for putting SGLLC in receivership – however, it is this very Receivership and the pending Motion to Clarify that has precipitated the foreclosure action by disrupting SGLLC’s ability to collect amounts owed for the continued storage of Uncle Nearest inventory.”

Say it with me folks- A business Keith owns, is owed money by a business that Keith manages, and has an equity stake in via another company Keith owns, is in financial trouble because it cannot blood suck more money out of the Uncle Nearest piggy bank. That’s not a business model. That’s leeching other peoples money. This is what commingling looks like.

“First, the Receiver has not paid the storage fees that are due to SGLLC and accrue at the rate of $6,500 per month, while SGLLC has continued to pay the costs associated with storing the inventory of the Uncle Nearest Entities in an approximately 25,000-square-foot climate-controlled facility.”

Poor Shelbyville Keith. He negotiated with UN Keith for $6,500 a month, and now UN Keith can’t pay.

“SGLLC provides this storage in the same manner as any climate-controlled storage provider, storing the inventory of the Uncle Nearest entities for a fee. Those inventory items include pallets of Uncle Nearest glass bottles, which must be stored in climate-controlled space to prevent molding, as well as used barrels, bottle labels, bottle closures, shipping cases, and bottle corks. Additionally, delayed payments from the Receiver on unrelated obligations, with adverse credit implications, have made matters worse. This has caused a cash flow issue for SGLLC, resulting in the need to liquidate assets to satisfy its obligations.”

Pardon my French for a moment, it’s about to be rankin. Uncle Nearest has a shit ton of land at the NGD compound. Why is it paying a Weaver entity a monthly fee to store shit when it could store it on property it already owns? Answer- because it’s a way to further leech money out of the company and into the Weaver’s coffers. Now that the UN spigot has been turned off, OPERATION CLEAN OUT UNCLE NEAREST has concluded.

“The pending foreclosure relates to a loan requiring refinancing due to a balloon payment. SGLLC would ordinarily refinance the loan or sell the property to satisfy that obligation. However, the uncertainty created by the Receivership and the allegations in the Motion to Clarify have made refinancing or sale impossible. Potential lenders and purchasers have required assurances that the Receiver will not attempt to unwind transactions involving SGLLC assets while the Motion to Clarify remains pending – assurances that cannot presently be provided.”

It’s funny how when you cannot pay your debts, and you end up in receivership, and the free flowing other peoples money dries up, that lenders wasn’t collateral that isn’t encumbered. Fear not, Alex Pineda will likely ride to the rescue.

“This is something that would never have been contemplated but for the confusion created by the Motion to Clarify as to the Non-Parties, and especially SGLLC.”

Put simply, we would have continued to fleece UN to keep our stuff, had it not been for this silly old receivership.

“While SGLLC has a plan for resolving the foreclosure, the foreclosure possibility cannot and should not serve as a basis for expanding the Receivership when the circumstances giving rise to that risk were themselves caused by the Receivership and the Motion to Clarify. To the extent that the Receiver has conjectured (with absolutely no evidence) that the property was “likely” acquired or maintained with funds from Uncle Nearest, that is absolutely false. There is literally no evidence to support the Receiver’s statement. SGLLC requests that the Court base any decision in this matter on facts, not the Receiver’s conjecture unsupported by actual evidence.”

Worry not, for UN funds WERE used in the acquisition and maintenance of these properties.

“Second, the pendency of the Motion to Clarify has caused SGLLC to be unable to sell its assets in order to alleviate the cash flow issue. Specifically, because the Receivership is a highly public proceeding and because the Motion to Clarify is pending, potential purchasers have required assurances that the Receiver will not seek to unravel any sale transaction relating to SGLLC assets. These two factors are the sole reason that SGLLC is dealing with a potential foreclosure. This unfounded Motion to Clarify has been and continues to cause extreme harm to SGLLC and needs to be resolved immediately.”

Folks, even without inclusion, the Seventies (TM) are finished. The loss of the passive income from Uncle Nearest is the cause, because like all Weaver companies, none of them are profitable, and cannot continue to exist without that cash infusion.

Aga in (TM)

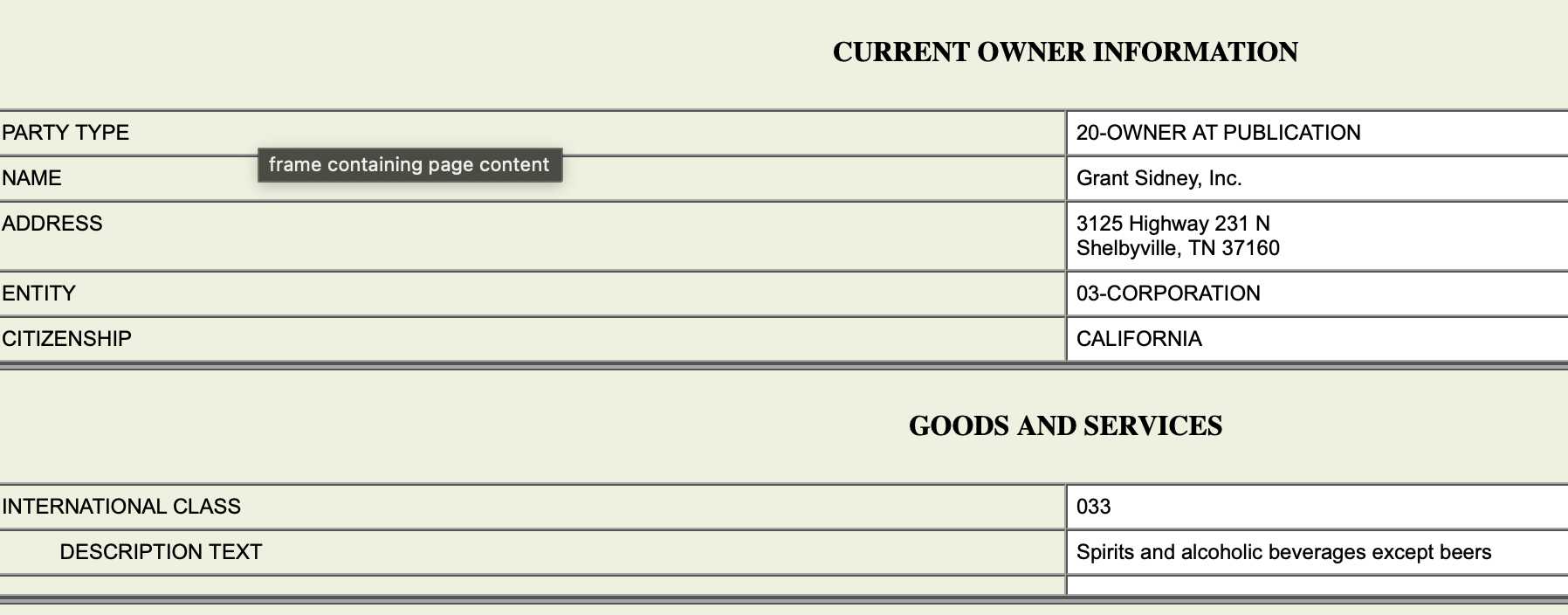

Last but certainly not least…… GRANT SIDNEY, not to be confused with The Weaver (TM) owned Sydney & Grant.

Let’s get this part out of the way -Receivership bad, not warranted, redefined commingling, no shared employees, copy paste….Also, The Weaver (TM) is big mad. Shall we?

“At no time were any of the funds used to benefit Grant Sidney or any entity other than the Uncle Nearest Entities. The Schedule 1.1 of the Subordinated Credit Agreement, which was created by Farm Credit, identifies specifically the payments that were made by Grant Sidney on behalf of the Uncle Nearest Entities during the relevant period. The fact that the funds ultimately came from MP-Tenn, LLC (“MP-Tenn”) is simply irrelevant to the question of whether there was commingling of the funds between Grant Sidney and the Uncle Nearest Entities.”

Heh, sure.

“The funds from this financing were never required to remain in any specific account, and the decision of Uncle Nearest to work with Grant Sidney as a de facto disbursing agent, to ensure the funds would be used for Uncle Nearest’s intended purpose, did not violate any law and was not fraudulent.”

I owe you $5. You’re right in front of me. My “friend” is next to me. I hand the $5 to my “friend.” My friend hands you the $5. Why the hell didn’t I just give you the $5 myself?

“That Uncle Nearest was intending to use the funds for the payment of its legitimate operating liabilities is not a fraudulent intent – in fact it is exactly the opposite of that.”

It didn’t make sense the first time she said it. Also, two mentions of not-fraud so far.

“Indeed, Uncle Nearest’s management of the funds, with the assistance of Grant Sidney, which was expressly countenanced by Farm Credit in its Schedule 1.1 to the Subordinated Credit Agreement, resulted in the funds being used exactly as they were intended.”

Again, why didn’t UN, who held the money, just pay the bank? Why did it have to pass through GS?

“Finally, the Receiver makes conclusory statements galore. The only true statement is that “all seven Related Entities are owned, managed, and controlled by Fawn and/or Keith Weaver. ” The rest is false. “

Cap’N Phillip told the truth one time, and everything else was a lie. Right. Got it.

“No fraud by Grant Sidney has been alleged with the particularity required for a federal pleading.”

Not Fraud counter is now at 3.

“The assertion that Uncle Nearest engaged in fraudulent conduct relating to the MP-Tenn transaction is not correct.”

Not Fraud counter is now at 4. Also, is this a Grant Sidney filing or Uncle Nearest?

We are at a crossroads folks.

“Although the transactions relating to the MP-Tenn convertible notes were complicated, the end result is: (1) that MP-Tenn loaned $20 million dollars to Uncle Nearest and Uncle Nearest received the full benefit of the $20 million loan.”

There’s a lot of reverse engineering of this deal here.

“Farm Credit has no standing to assert that Uncle Nearest acted fraudulently with respect to MP-Tenn and has no knowledge of the specific communications between Uncle Nearest and MP-Tenn relating to the transaction.”

Not Fraud counter stands at 5.

“MP- Tenn was fully aware of the circumstances underlying the convertible credit agreement and the intention was that the loan would be converted to equity and never have to be repaid. That would likely still be the case but for the Receivership.”

The Weaver (TM) insanely picked Jay-Z’s pocket, and is now blaming it on the receiver? When the lawsuit began, MarcyPen demanded payment. They probably didn’t know it at the time, but that money was gone in the forever hole.

“The decision of Uncle Nearest to direct the funds received from MP-Tenn to Grant Sidney as disbursing agent was a proper exercise of business judgment made on the advice of legal and financial counsel.”

Well, those folks were idiots, and if they weren’t, they took too many hits to the head by a cast iron frying pan to offer sound advice. No idea what the excuse is for The Weaver (TM) for following said advice.

“Since the MP-Tenn funds were earmarked for certain expenditures, the use of a disbursing agent to ensure the funds were used for the required purpose was entirely appropriate, and the funds were disbursed exactly as required.”

No matter how many times The Weaver (TM says this, it still never makes any sense.

“ Farm Credit’s further insinuation that a Company managing for tax liability is improper is simply naïve. It is entirely appropriate for a Company to consider the tax implications of transactions in advance and to structure transactions to reduce tax liabilities where prudent. In this case, the structure of the transaction allowed Uncle Nearest to receive $20 million rather than the approximately $11 million it would have received had the transfer been structured as a direct sale of stock, so the transaction structure benefited both Uncle Nearest and Farm Credit.”

I’ll leave the Not Fraud counter at 5, but I thought this might’ve pushed it to 6. It’s so weird, that it was a loan, but then a stock sale, but then it wasn’t a stock sale because Grant Sidney’s share count never dropped, and oh come on with this gobbledygook.

“Farm Credit has produced no evidence of any fraudulent intent by Uncle Nearest, its management team, or Grant Sidney. “

Not Fraud counter is now solidly at 6. Can we get a 6-7?

“In the absence of fraud pleaded with particularity, Farm Credit’s allegations of fraudulent conduct should be ignored, struck, and dismissed.”

Not Fraud counter 7 and 8.

Aga in (TM)

We’ll keep it going with Grant Sidney, Fawn and Keith’s filing asking for the removal of the receiver. Lots of Receiver bad at his job blah blah blahs, so just the highlights.

“At the time the Receivership began, the Company was out of stock in only one limited market, and even there only with respect to a portion of the state served by a distributor with whom the Company was already in active negotiations to terminate its relationship. Outside of that limited market, there were no out-of-stock conditions when the Receiver assumed control.”

Another acknowledgment by The Weaver (TM) that the farcical Clear the Shelves campaign was an abject failure.

“The broader supply disruptions referenced by the Receiver did not arise until after the Receivership began and were tied to a change in terms imposed by the Company’s bottling partner, Tennessee Distilling Group (“TDG”), following the Receiver’s initial communications with that partner.”

Keep in mind that the relationship with TDG had been tenuous long before the receivership happened.

“Prior to the Receivership, the Company had an established arrangement with its bottling partner under which TDG continued bottling and shipping product while the Company paid federal excise taxes at the time of shipment and reduced legacy balances over time.”

I’m not broke, or in debt, I just have legacy balances. Man, if only Chase would let me make that distinction.

“Following the Receiver’s communications with TDG immediately after the Receivership began, those longstanding terms were no longer honored. “

Could it be that the reason TDG said “nah” was because they understand the severity of a receivership and that it means that they as a creditor is very low on the getting paid back totem pole?

“As a result, shipments that had previously flowed under the existing arrangement were halted until new payment terms were satisfied.”

Yes, TDG no longer was willing to operate under the previous TrustMeBro plan.

“The Receiver also asserts that the decline in sales is not evidence that the Receiver is not doing his job. That may be true, but it does evidence that the Receiver is either doing his job poorly or the Receivership itself is causing the poor performance.”

I’m sure that Cap’N Phillip is devastated by this critique of his performance from a former CEO who ran her company straight into receivership.

Context below.

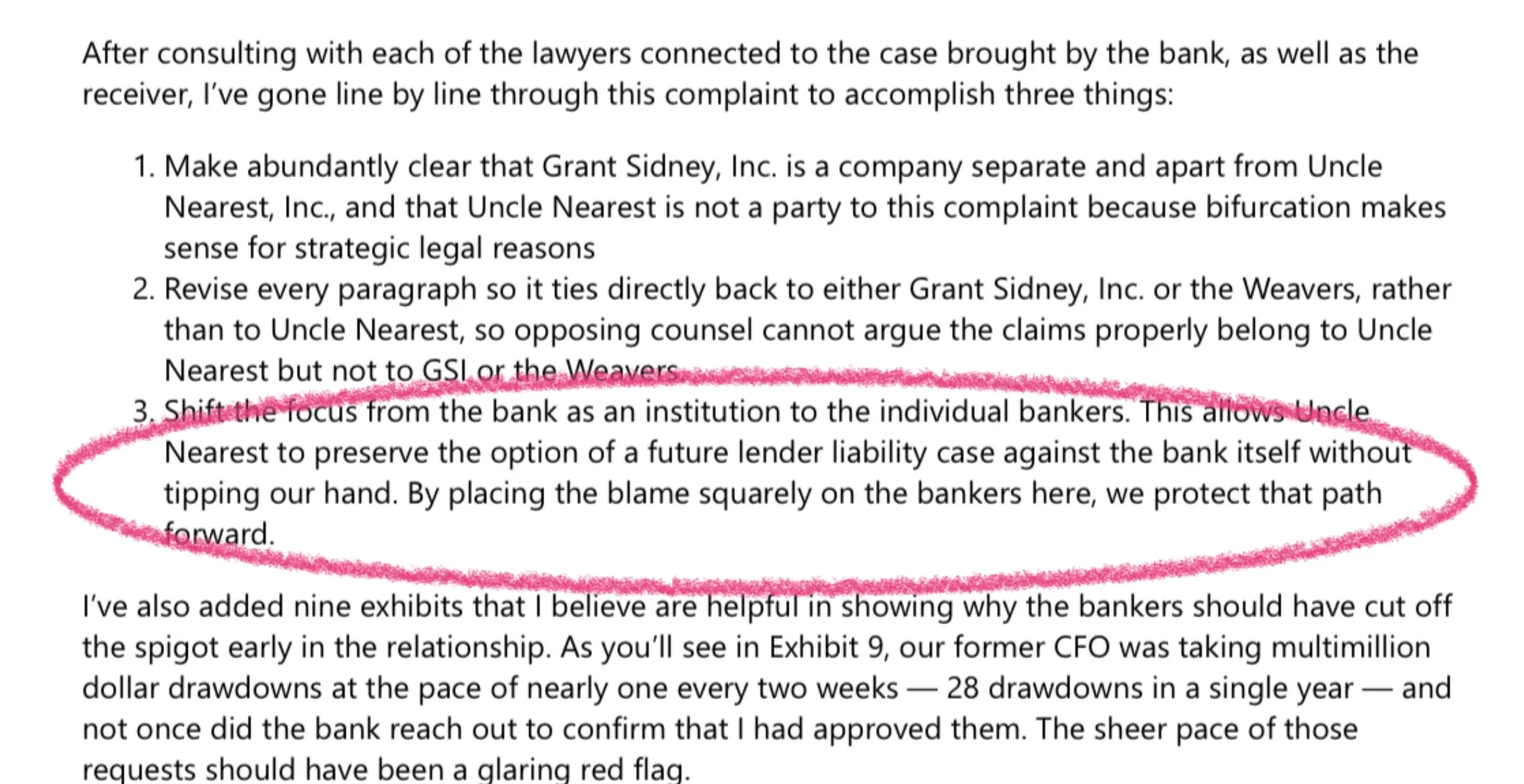

The image above is from an old filing. In that filing Michael Collins inadvertently included an email from The Weaver (TM) that was laying out the legal strategy for how to deal with the bank. I didn’t report on this at the time, but now seems an appropriate time, as The Weaver (TM) is about to attempt to execute on that strategy below.

They argue about the “correct” way to calculate solvency, and frankly I’m not interested in FawnMath (TM) so we will move on from there.

“Farm Credit’s analysis of the total debts includes disputed debts and includes the Advanced Spirits debt which is offset by the Advanced Spirit barrels.12 Consequently, the total debt is significantly less than that asserted by Farm Credit.”

Sure sure, it’s not a metric shit ton of debt, just a standard shit ton.

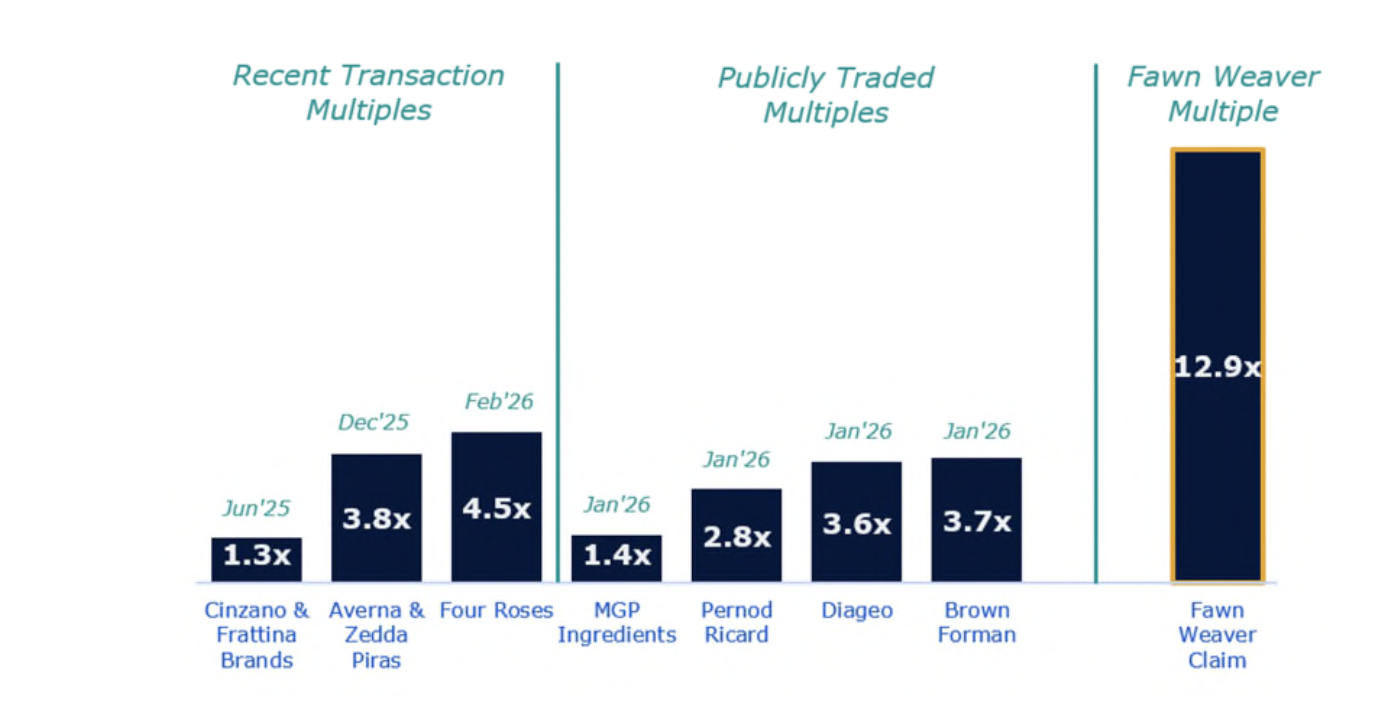

They bring up some gibberish about Four Roses. It hurt my head to read it, no way I’m typing it. It’s really irrelevant, billable noise.

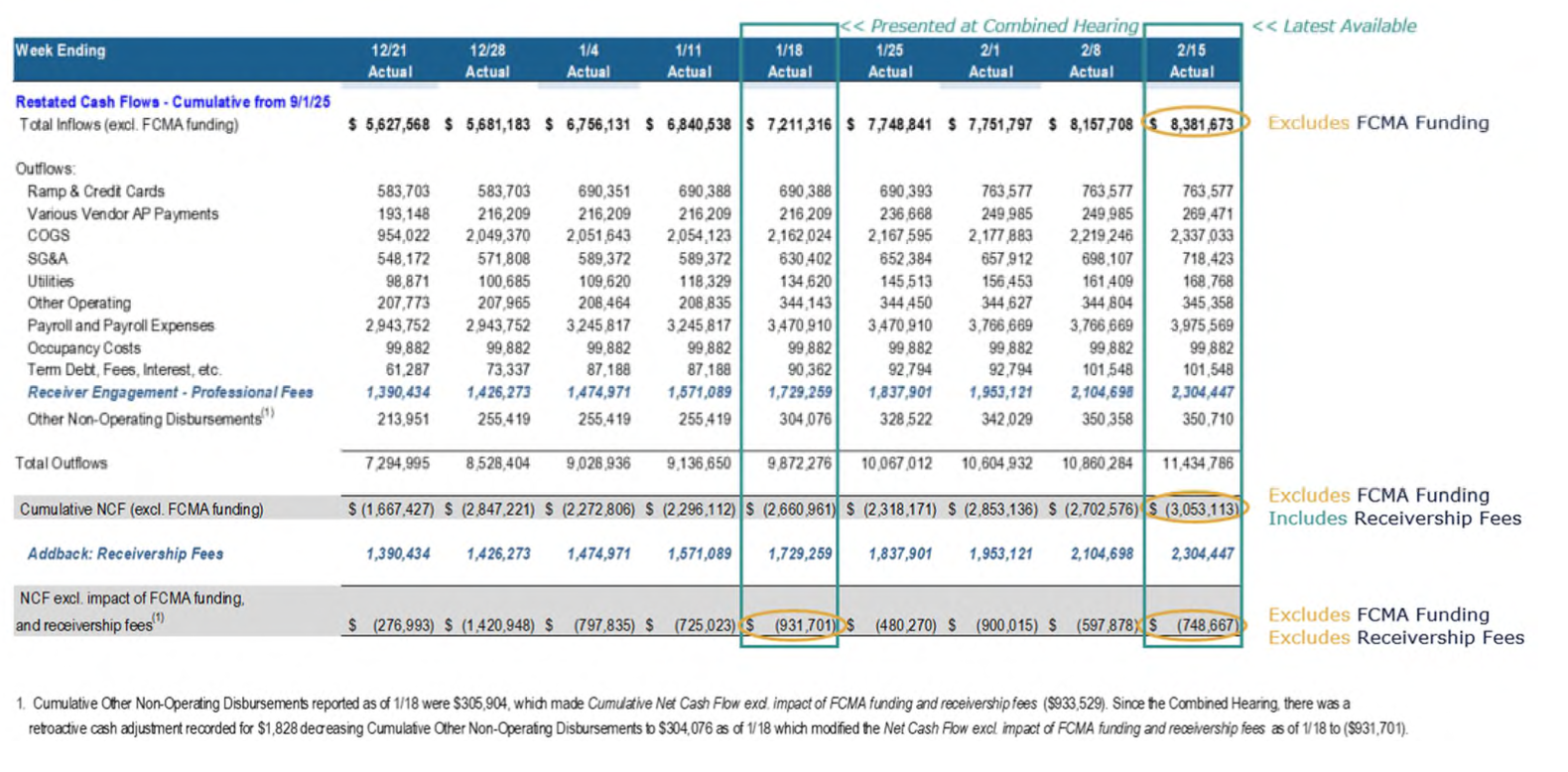

“The assertion that, but for the Receiver, Uncle Nearest would have been cash flow negative by $16 million over the period September 1, 2025, to January 18, 2026, is ludicrous. It is literally impossible to have a negative actual cash flow.”

You know how people love to say “Failure is not an option?” Failure is always an option, it’s just not a desired option. Negative cash flow is just a polite way of saying you spend more than you earn. When I’m in Las Vegas (and I don’t gamble mind you), I am ALWAYS negative cash flow. Literally.

“A company can project a negative cash flow in the future, but it can’t have actual negative cash flow. A company can only disburse the cash it has – if it doesn’t have cash, it can’t have disbursements.”

I didn’t see a citation for Business For Dummies.

“If a company’s ability to meet its debts as they come due requires that company to have the cash immediately to completely pay off its long and short-term debt, then practically every company in America would be presumed insolvent.”

Not how it works, but please, go on.

“The evidence is clear that the Company has and can continue to operate in a cash flow positive manner once the Farm Credit funding is removed, and the payments to the Receiver ($2.3 million) and to Tennessee Distilling Group ($1.5 million) are added back. As explained in the Movant’s Post-Hearing Brief and as supported by the evidence, the Company is, and is expected to remain operating cash flow positive by approximately $900,000 through April 2026”

Recall that the bank, and the receiver both have disputed FawnMath (TM).

“ In fact, Farm Credit’s financial advisor admitted that if the borrowing base were calculated and achievable at 100% of the barrel cost, then the value of the barrels would cover the loans. That is evidence that Farm Credit has adequate security.”

That’s a big big IF in this market where aged MGP can be purchased VERY cheaply.

“Additionally, there is no evidence that the value of the assets is declining. The whiskey barrels continue to age and become more valuable over time. Additionally, the current glut of whiskey in the market is beginning to clear up as most distilleries have cut back new production such that the improvement in the overall market is inevitable as demand begins to catch up with supply.”

Beginning to clear up? Dear lord, we aren’t even at the end of the glut yet.

“Farm Credit’s assertion that there are no less drastic equitable remedies available is incorrect. First, Farm Credit ignores that, for more than 8 months after Farm Credit ceased providing capital to Uncle Nearest, the Company was able to continue to grow sales and had arrangements with its key vendors. As Farm Credit is well-aware, the Company had engaged multiple legal and financial advisors in order to address the issues that were created by the Company’s prior CFO, and those efforts were progressing.”

Finally a Blame Senzaki moment. Also, the sales numbers were continually made up after Mike was gone.

I like to periodically remind folks that this guy Oren is on the team that doesn’t represent the Weavers.

“The draft of the lawsuit against the Company’s CFO was shared with the Receiver in his very first meeting with Ms. Weaver following his appointment, which she followed up with sharing in email form, along with the exhibits, only days later. The Company’s management team had been working to resolve the issues through its engaged professionals literally until the day the Receiver was appointed. That effort stopped because the Receiver required it be stopped by advising all of the Company’s advisors to stand down so that the Receiver’s advisors could take over. Unfortunately, this has likely led to a significant amount of duplicated effort.”

Or his work was able to find a different narrative.

“In sum, the Company’s management team is well-positioned to take back over full operations and put the Company back on a growth trajectory, which will improve cash flow and improve the Company’s enterprise value for the benefit of all of the creditors and shareholders.”

Noted person that has a proven history of being unbothered and unmoved about not paying bills to businesses small and large for years, thinks that the court will believe that only she can save Uncle Nearest.

“The assertion that Uncle Nearest engaged in fraudulent conduct relating to the MP-Tenn, LLC transaction is not correct. “

Not Fraud counter is now at Eleventy (I’m using FawnMath now).

“Furthermore, the Receiver has now billed the estate more than $2.3 million, and the rate of expense appears to be increasing. However, the Receiver literally has nothing to show for the efforts except a slew of accusations without any supporting facts or evidence put on the record. He has asserted that he has not been able to get the financial records sorted out. He hasn’t been able to get the cap table figured out, and he hasn’t done any investigation of the transactions related to the Non-Parties. His only accomplishment for $2.3 million in fees is overseeing the massive decline in the Company’s sales, which is resulting directly in his inability to find investors willing to refinance the debt or invest market price for the brand.”

I wonder why he can’t get the records or cap table sorted? Perhaps it’s because of the former Peoples CEO malfeasance?

“Next, allegations were advanced suggesting misappropriation of $2.2 million to acquire property in an “exclusive enclave of Cape Cod” – i.e. the Martha’s Vineyard Property. The record reflects that:

(a) The purchase agreement for the MV Property had been provided to Farm Credit more

than one month before closing;

(b) The structure of the transaction was known to and supported by Farm Credit;

(c) The property operated as the “Uncle Nearest House on the Vineyard” with a clear

marketing purpose for Uncle Nearest; and The $1.5 million loan relating to the MV Property corresponded to documented renovation and lot consolidation costs that were made to the MV Property.”

The bank has never said they didn’t know about the damn house. Why do they keep asserting this? The bank knew the loan was going to the MV purchase, and what the intended purpose was. They didn’t know Keith would turn around and mortgage their collateral though.

Goals.

“Contemporaneous evidence further confirms that the MV Property and its purpose were known to Farm Credit well before the present dispute.”

Evidence confirms that water is wet, and that the bank knew about the property. Both are known facts, and aren’t in dispute.

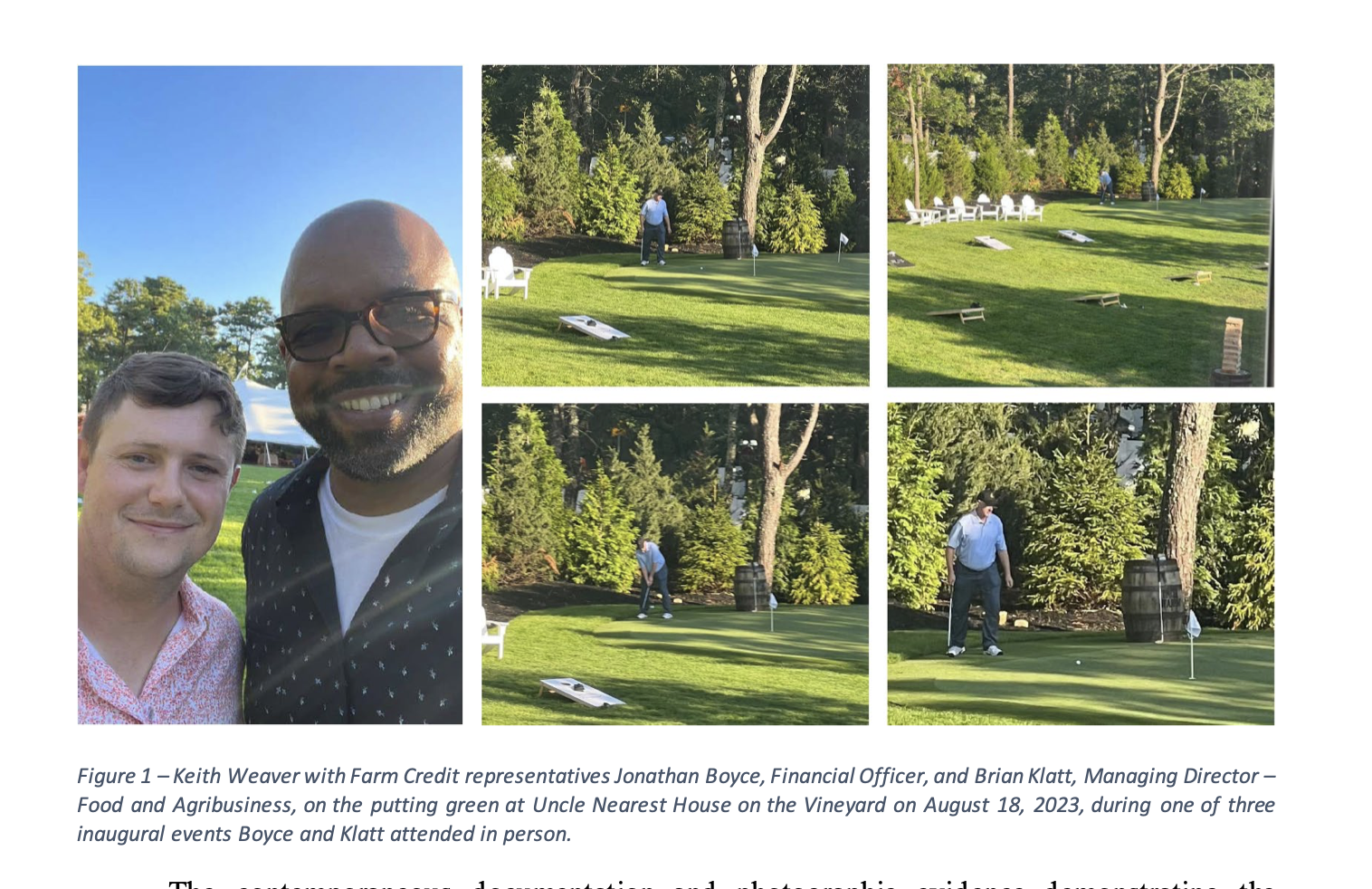

“Photographs, shown below, from August 18, 2023, show Farm Credit personnel, including Jonathan Boyce — the bank officer responsible for countersigning Uncle Nearest drawdowns on its credit line — and Brian Klatt present at the MV Property during company-related events. These images depict lender representatives on the property grounds, including use of the outdoor recreational facilities. The photographs are consistent with the documentary record demonstrating that the existence, ownership structure, and use of the MV Property were contemporaneously known to Farm Credit, long before the purchase was later intentionally mischaracterized by Farm Credit in litigation filings as “misappropriation.”

Remember that email that was included erroneously in an earlier filing by Michael Collins? This is the strategy in action. Shift it from the bank, and onto the people at the bank.

“After Movants placed the relevant documentary evidence on the record, the misappropriation theory was not pursued by Farm Credit in the same form. As the record clarified the MV Property issue, Farm Credit’s filings moved on to the next alleged “headline” misconduct narrative.”

That’s not exactly how that happened. The bank never disputed the purchase. They disputed that the house was then mortgaged to another bank,

Hey look, a bank dude playing golf with Keith. Looks like a nice day. So what?

“The contemporaneous documentation and photographic evidence demonstrating the lender’s awareness of the MV Property and its use underscores a recurring theme throughout these proceedings: allegations advanced by Farm Credit in this litigation that were inconsistent with facts already known to Farm Credit at the time.”

I have never hated the misuse of the word “evidence” more than I have today, after reading The Weaver (TM) repeatedly infer that it’s “proof.” I have evidence of Bigfoot, but it is not proof, mainly because I ate a bag of Jack Links back in the day.

“The Receiver has since expanded the narrative further, conjecturing that Company funds were “likely” used to purchase assets for the Non-Parties, with no evidence to support that allegation. No tracing analysis or documentary evidence has been identified demonstrating that any Company funds were used to acquire any property not for the benefit of Uncle Nearest.”

Notice the last line which I bolded. This statement doesn’t say UN funds weren’t used to acquire property, it says that if it was done, it was for UN’s benefit, which is to say, benefited the owners.

“Prior to the Company’s formation, they held more than $2.5 million in real estate assets, generated annual income in excess of $1 million, and had invested more than $2.5 million in other founder-led companies.”

That’s all? Also, pretty sure that $1 million was Keith’s Sony money.

“At a minimum, the series of allegations that are demonstrably false, along with allegations unsupported by any evidence, support a finding that Farm Credit has unclean hands in this proceeding and is no longer entitled to equitable relief. Likewise, the Receiver’s repeated advancement of materially incomplete or contradicted allegations has undermined confidence in the neutrality and candor required of a court-appointed fiduciary.”

I’ve said this many a time- She is hell bent on suing this bank.

“ Movants respectfully submit that any determination relating to the requested termination of the Receivership Estate should not be based on the Receiver’s or Farm Credit’s conjecture but on the actual documentary evidence presented. Movants reserve all rights to seek appropriate relief should further proceedings confirm that material facts were knowingly mischaracterized or withheld.”

Everyone is lying but The Weaver (TM) oh and also she wants to sue the bank.

The Meowvants (TM) obviously are against inclusion, and for promoting Cap’N Phillip to customer.

The life of a “distillery” cat.

UPDATE 3/7-

Before we get to the Meowvants (TM). I have a bombshell that I’ll try to fit in here.

If you don’t watch Kandi on TikTok you really should. She’s always quotable and funny. So allow me to drop this here, with some Kandi spice.

Allegedly, HIPAA violation HIPAA violation, A certain board of directors member Allegedly of Uncle Nearest is rumored to have Allegedly HIPAA violation HIPAA violation hired a very, very, very expensive law firm. Allegedly.

I will not elaborate further at this time.

I’ll be back shortly with an update on the Meowvants (TM) filings. I apologize for the delay.

Inclusion is coming.

UPDATE #2- 3/6-

Now we get to the Farm Credit filing in regards to inclusion.

“As an initial matter, while FCMA continues to support the Entity Clarification Motion, FCMA is not the movant and bears no burden in connection with the Entity Clarification Motion. Any burden rests with the Receiver and arguments in the Additional Entities’ Supplemental Briefs to the contrary are incorrect.”

“Further, the Additional Entities continue to egregiously mischaracterize both the Grant Sidney transaction and FCMA’s knowledge of the details.”

“Lastly, putting an end to these unmeritorious filings is in the best interests of the receivership estate, Uncle Nearest, creditors, and other stakeholders. Without the constant flurry of filings necessitating responses and hearings, the Receiver can focus his full attention on managing the receivership estate, operating Uncle Nearest efficiently and preserving assets. Accordingly, FCMA maintains that the receivership should be expanded to include the Additional Entities as Receivership Assets due to the extensive evidence of commingling both on the record and presented at the February 9, 2026, hearing.”

I’m staying out of the kitchen here, and letting the bank lawyers cook.

“The Additional Entities each argue that FCMA bears the burden of piercing the corporate veil to prove that the entities are alter egos of Uncle Nearest under Tennessee law. This argument is incorrect. The party wishing to pierce the corporate veil bears the burden of proving facts sufficient to justify piercing the corporate veil. The Receiver, not FCMA, filed the Entity Clarification Motion. As a result, while it does not bear the burden of proof, FCMA hopes that its pleadings lend further support to the Receiver in meeting his burden.”

The oil is hot…..

“Grant Sidney and Fawn Weaver (“Ms. Weaver”) continue to mischaracterize the “sale of approximately $20 million of Ms. Weaver’s personal shares”11 and now Ms. Weaver declares that FCMA knew of the source of the funds (which it did not) Grant Sidney infused into Uncle Nearest in early 2025. FCMA permitted what it believed to be a loan from Grant Sidney to Uncle Nearest to ensure continued operation and debt repayment. FCMA required and insisted upon a subordination agreement to confirm that any loan other than FCMA’s debt would be subordinate to the FCMA debt. Though Grant Sidney argues the Subordinated Credit Agreement evidences separate legal existence between it and Uncle Nearest, before its execution, Grant Sidney loaned $12,526,270.00 to Uncle Nearest over the course of two months in 15 separate transactions without any written agreement.”

The meat is being seared.

“Despite fully admitting that Ms. Weaver moved funds from Uncle Nearest to Grant Sidney to conceal assets from FCMA, the Weaver Parties now seek to recharacterize the transactions.”

Little bit of rosemary…..

“Ms. Weaver misrepresents that “[t]he structure of the funding through the Grant Sidney account was known to and approved by Farm Credit.” Ms. Weaver further misrepresents that FCMA was “fully aware of and consented to the transaction being made through Grant Sidney.”15 Ms. Weaver states the account Uncle Nearest used to effectuate the transaction was “subject to Farm Credit’s monitoring and full visibility.”16 The Weaver Parties attempt to imply (incorrectly) that FCMA was in no way misled at the time. FCMA was considerably misled.”

The meat is flipped…..

“These assertions ignore many omissions on the part of Ms. Weaver. Ms. Weaver and Grant Sidney omit that FCMA (a) was not made aware of the loan from MP-Tenn, LLC,17 (b) was not made aware of the “new Uncle Nearest Business Money Market Account (Account No. ***873)18 and (c) did not have access to or “full visibility”19 into the Grant Sidney Account No. ***881 at the time of the Forbearance Agreement.”

Adding in some butter….